The stock market is a powerful tool to save for retirement and grow wealth. Learn the nine important steps to get into stocks.

While the stock market isn’t for everyone, it’s still a powerful tool to grow your retirement savings, protect you from inflation, and build wealth. You don’t need to spend a lot of time or invest a lot of money to get started.

Step 1: Set Your Goals

Your first step is to determine your financial goals. Yes, we all want to “make loads of cash,” but your financial goals should go deeper than that.

Ask yourself if there’s room in your current budget for investing. If you spend all of your cash on legitimate expenses each month, you should first work on boosting your income. If you have a lot of debt, it’s usually smarter to pay down your debt first.

Then ask yourself why you want to invest in the stock market. Do you want to save for retirement? Do you hope to pass an inheritance down to your kids? Do you want to grow your children’s college savings? Why you invest will influence how you invest.

It’s also okay if you decide that now isn’t the right time to start investing. Generally speaking, it doesn’t make sense to buy stocks with money you’ll need in less than five years. A sudden downturn could erode your balance. If you plan to have a baby or buy a house next year, for instance, it’s smarter to load your cash into a high yield savings account.

There are no right and wrong answers here, but it’s important to be honest with yourself. Your answers will shape your investment strategy.

Step 2: Establish an Emergency Fund

An emergency fund is a cash reserve you keep on hand at all times to handle unexpected costs. It’s for when your furnace breaks in the winter, you have to purchase a last-minute flight, or you suddenly lose your job.

Your emergency fund needs to be liquid (easy to access) and large enough to cover life’s challenges—including months without work. If you withdraw money from your investing account to pay for these expenses, there’s a good chance you’ll lose out on growth and pay hefty fees.

How much should you keep in your emergency fund? That depends on your expenses, but most financial planners recommend keeping three to six months of income on hand at all times. It should be enough to pay for all of your expenses during that time period, including debts. Keep it in a savings account you can access at any time and refill the balance if you use any of it.

Step 3: Learn About Investing

When it comes to investing, knowledge is your most powerful tool. You’ll need to learn everything you can in order to buy stocks safely. Your first step is to start consuming financial news. You may not understand all of the terms, but you will get a sense of markets and how they behave.

Next you’ll want to dive into some deliberate study. Start with Wealthsimple’s Investing Master Class to gain a foundation of personal finance and investing knowledge and learn how to build real wealth with time-tested advice.

Then move into Personal Finance 101, a massive resource to help you understand the art of managing your money. This is a great place to find answers to your specific questions.

Risk is an inherent part of investing, but you can reduce your risk by educating yourself.

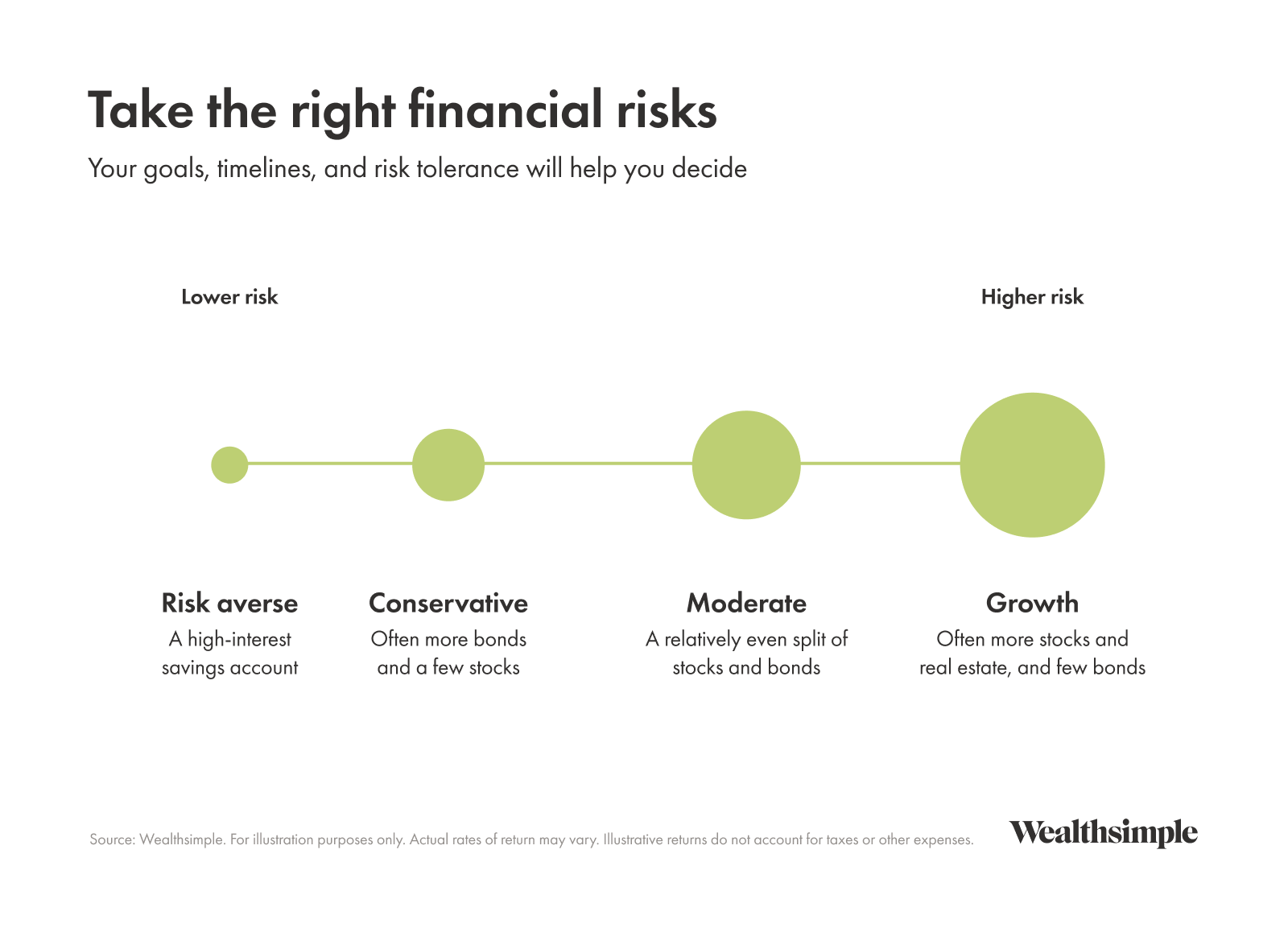

Step 4: Understand Your Risk

While it’s possible to raise or lower the risk of investing, it’s not possible to eliminate it entirely. Every stock you purchase will come with some risk, even if that stock has behaved predictably for a long time.

The calculus is fairly straightforward: Stock with higher growth potential generally come with more risk. Safer stocks typically come with modest growth. Smart investing means balancing your risk at a comfortable point between safety and growth.

Most people evaluate their own risk tolerance based on their age. Younger people usually opt for more risk and more growth. Older people, who expect to use that money for retirement, typically choose “safer” investments that don’t risk their savings.

However, some people, no matter how old, just don’t like risking their money, so they always opt for conservative investments. Other people always want growth. What’s important is that you know what’s right for you.

Step 5: Choose Your Investing Style

Your investment style affects what you’ll buy, how you’ll buy it, and whether someone will manage your portfolio on your behalf.

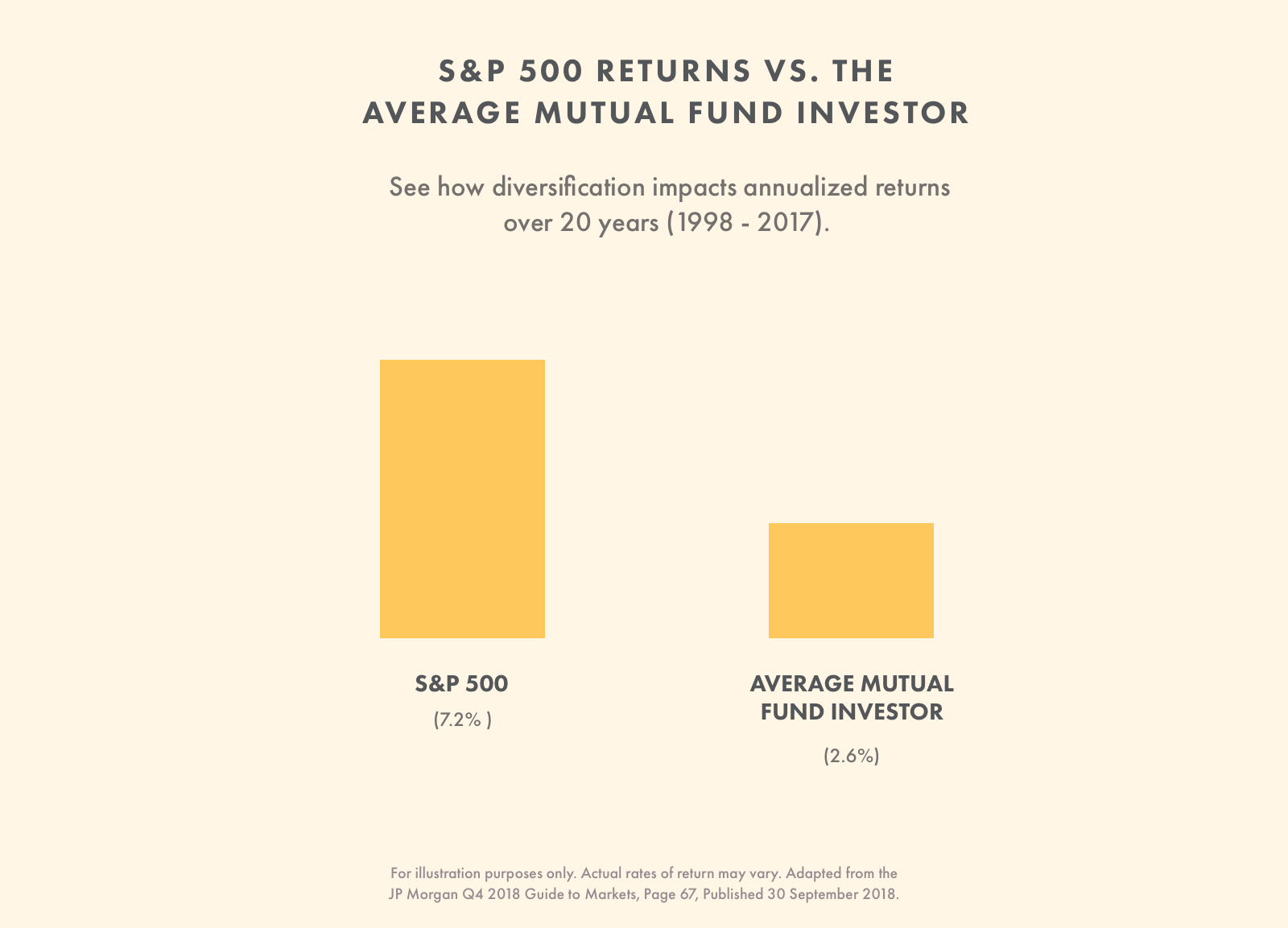

First, choose an active or passive management style. Active management means you (or someone else) will buy stocks or funds to try and beat the market. Passive management is when you buy funds that track a benchmark, which means there’s little for a manager to do.

It means you’ll build a reasonable portfolio and hold it for the long term. Keep in mind that numerous studies have shown that most actively managed funds fail to “beat the market,” especially when you consider their higher costs.

Next, decide if you want a Wealthsimple Trade portfolio or a managed portfolio. Trading means you’ll do the work yourself. Managed means you’ll outsource the work to a person or service.

If you invest with Wealthsimple, for example, you’ll engage in a passive investment style with a managed portfolio. You make a few basic choices and we do all the work.

Step 6: Choose Your Investing Account

Now it’s time to take action by opening your investment account. This is where you’ll place all of your investment to (hopefully) grow over time. The best part is that these accounts have tax advantages. You don’t pay taxes on the money you contribute (to a limit), but you can’t withdraw money too early without paying penalties.

The best place to begin investing is a retirement account. In the United States, this would be either a 410(k) through your employer or an IRA (traditional or Roth). Canada, you have the Registered Retirement Savings Plan (RRSP). In the UK, you can open an Individual Savings Account (ISA).

Employer-sponsored accounts are especially attractive if the employer matches a percentage. For instance, an employer might match up to 3% of your salary, which means you get a guaranteed 3% plus the account’s performance. The downside, however, is that you rarely get to choose how the money is invested. Other accounts that aren’t tied to your employer give you more control over what you own.

If you’ve maxed out your contributions to a tax-advantaged account, your remaining option is a taxable account. You can deposit as much money as you like into this account and there are no penalties for withdrawing money. The downside is that you’ll have to pay taxes on whatever you earn.

Step 7: Open an Account with an Investment Provider

An investment provider is simply a brokerage that helps you buy and sell stocks (and other securities) on the market. They are not all the same. You’ll need to choose the one that’s right for you. Fortunately, you can do this all online without paying a lot of money.

Do some quick comparison shopping to find the investment provider that’s right for your situation. If you plan to purchase stocks individually, you’ll want a broker that lets you create your own portfolio. This broker should provide educational features, reports, news, etc.

But if you don’t want to pick your own stocks and you’d prefer to let experts and automations do the leg work, you’ll want a robo-advisor (like Wealthsimple) that uses computer algorithms to manage your portfolio, including automatic rebalancing and tax optimization. These come with less choice, but less work and far lower costs.

Step 8: Understand Diversification

Diversification is a critical component of a sound investment strategy. It helps you manage risk, preserve your capital, and achieve steady growth. (No guarantees, of course, but these benefits are well documented.)

What is diversification? Basically, it means buying a lot of different securities rather than pouring all of your money into a single investment. When you own a lot of things, poor performance by one of them won’t do much damage to your portfolio. But if you only own one thing, a bad year could wipe you out.

How do you diversify? The easiest way is to purchase mutual funds and exchange traded funds (ETFs) rather than buying individual stocks. These securities come with built-in diversification because they pool investor money together to buy many stocks.

If you choose to buy individual stocks, spread out your money as much as possible. Purchase many companies (after careful stock research) in different sectors and industries. Don’t rely on just stocks, as well. Put some of your money into bonds.

Step 9: Fund Your Account to Start Investing

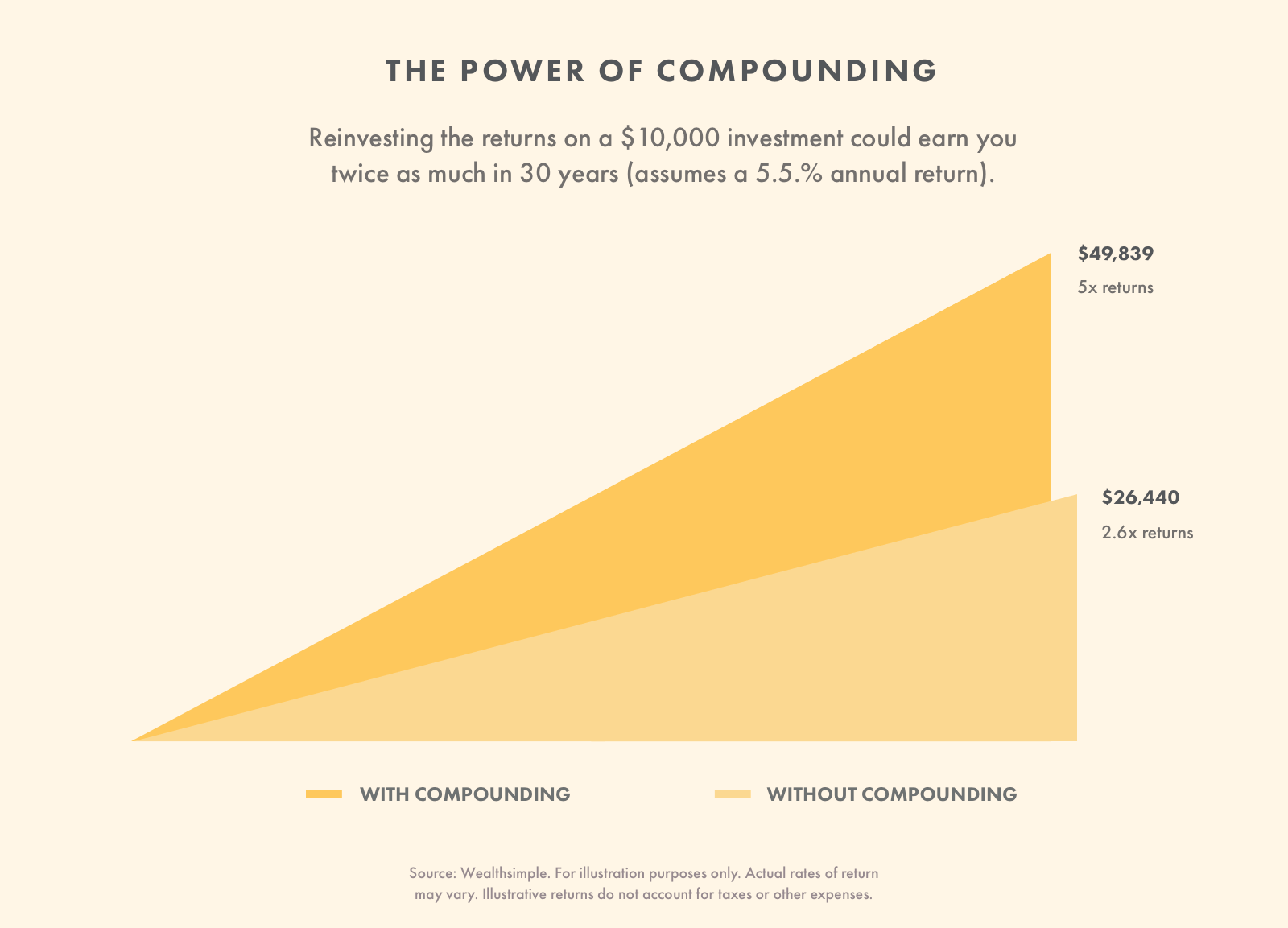

Your final step is to start funding your investment account. There’s no right or wrong way to do this, but to take advantage of compounding interest, you’ll want to put as much money as you can into your investment accounts as you can. It’s better, for instance, to make monthly contributions to your retirement account rather than dumping in the maximum at the end of the year so your money earns interest throughout the year.

No Secret Formulas

Despite what some gurus would tell you, there’s no magic formula to achieve wealth through the stock market. Learn as much as you can, fund your accounts as often as you can, and avoid checking your portfolio every hour. If you do all that, there’s no reason you can’t be a successful investor.