Besides market fluctuations and interest rates, there is another factor that can affect the returns from your investments: taxes. Tax-efficient investing is a strategy that aims to minimize the taxes you pay on investment gains, helping you keep more of what you earn.

How your investments are taxed depends on two things: the type of income they generate — interest, dividends, or capital gains — and the account you use to hold them, such as a Tax-Free Savings Account (TFSA), Registered Retirement Savings Plan (RRSP), or a non-registered account.

This article covers how investment income is taxed in Canada, strategies for reducing your tax burden, and how to match the right investments with the right accounts.

How investment income is taxed in Canada

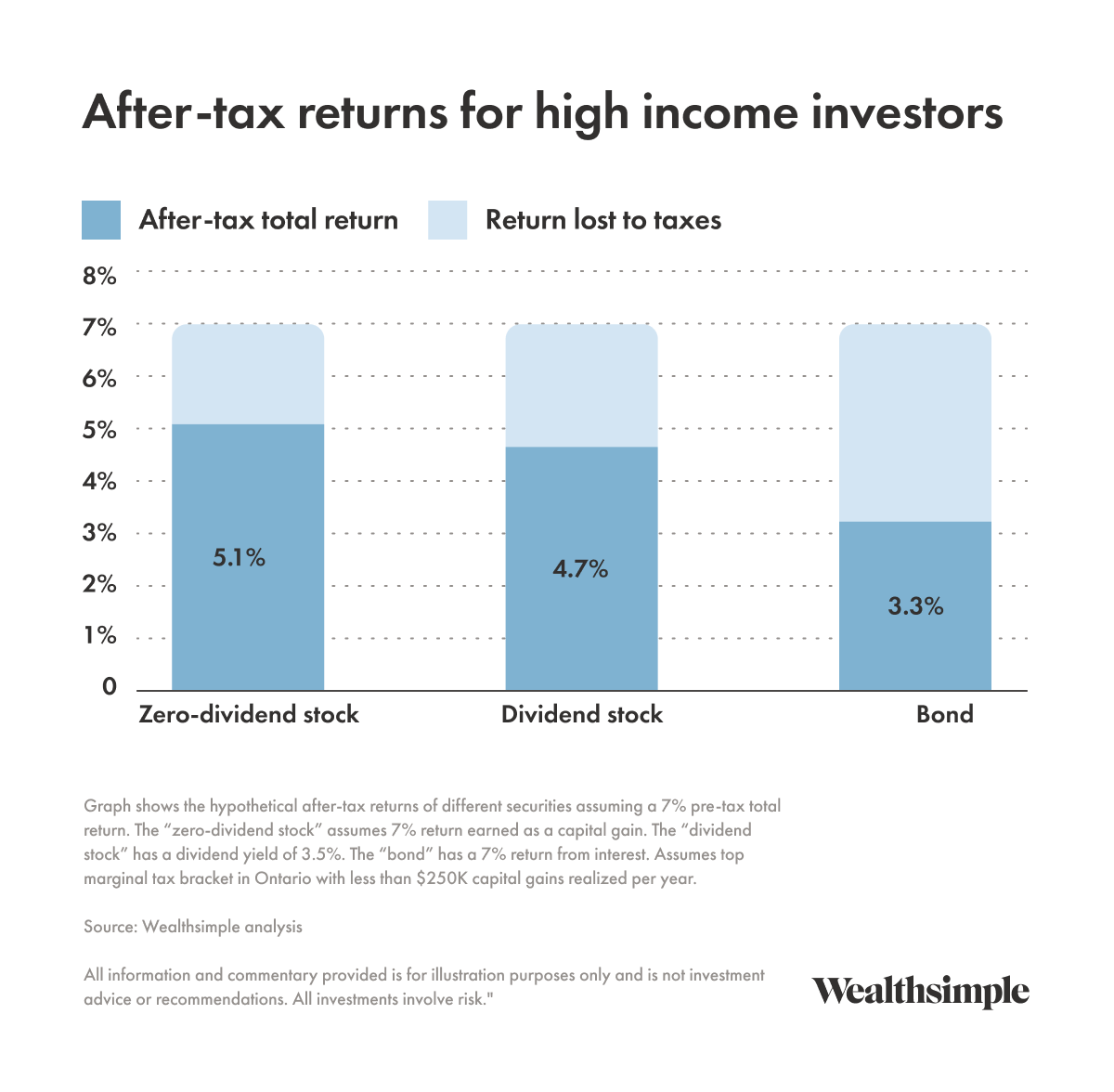

In Canada, investment income falls into three categories — capital gains, dividends, and interest — and each is taxed differently. Capital gains are the most tax-efficient, followed by eligible dividends, then interest income. Understanding these distinctions is the foundation of a tax-efficient investing strategy.

Capital gains

A capital gain occurs when you sell an investment for more than you paid for it. Only a portion of the gain is included in your taxable income, making capital gains the most tax-efficient form of investment income in Canada.

As of 2026, capital gains in Canada are included in taxable income at a rate of 50%.

Dividends and the dividend tax credit

The dividends you earn as a shareholder in a company are taxed differently from capital gains. If you own shares in a Canadian company, you may be eligible for the Dividend Tax Credit, which helps offset double taxation on corporate profits already taxed at the company level.

Eligible dividends — typically paid by larger, publicly traded Canadian corporations — receive a more generous tax credit than non-eligible dividends. Canadian dividends are often taxed at a lower effective rate than interest income, though generally at a higher rate than capital gains.

Interest income

Interest earned on investments such as bonds, Guaranteed Investment Certificates (GICs), and savings accounts is the least tax-efficient type of investment income. Interest is fully included in your taxable income and taxed at your marginal tax rate, with no special credits or reductions available.

Strategies for tax-efficient investing

Tax-efficient investing is based on the types of investments you choose, the accounts you use, and how you manage your portfolio over time. Here are several approaches that can help reduce your overall tax burden.

Tax-aware asset allocation

Tax-aware asset allocation means choosing a strategic mix of assets that helps you diversify while minimizing the effects of taxes. Some asset classes — such as bonds, stocks, cryptocurrency, or hedge funds — offer similar diversification properties but generate different types of income.

Choosing asset classes that produce more tax-efficient income can reduce your overall tax bill.

Choosing the right account type

Deciding which accounts to hold your investments in can make a meaningful difference to your after-tax returns:

TFSA: Returns on most investments are tax-free, meaning your income or gains are maximized.

RRSP or First Home Savings Account (FHSA): Taxes on any gains or income are deferred — you will not pay taxes until you withdraw money from the account.

Non-registered account: All investment income is taxable in the year it is earned or realized.

Account selection is one of the most impactful decisions in a tax-efficient investing strategy.

Tax-aware security selection

If you are investing in international stocks, some account types may offer tax credits or reimbursement for taxes paid abroad. Dividends paid on U.S. stocks are subject to a 15% withholding tax in Canada, but certain accounts — such as an RRSP — can eliminate this tax under the Canada-U.S. tax treaty.

Tax-loss harvesting

Tax-loss harvesting is a strategy where you sell an investment that has lost value and use the loss to offset capital gains elsewhere in your portfolio. You cannot buy the exact same security back within 30 days — doing so would trigger the superficial loss rule — but you can purchase a similar investment to maintain comparable diversification.

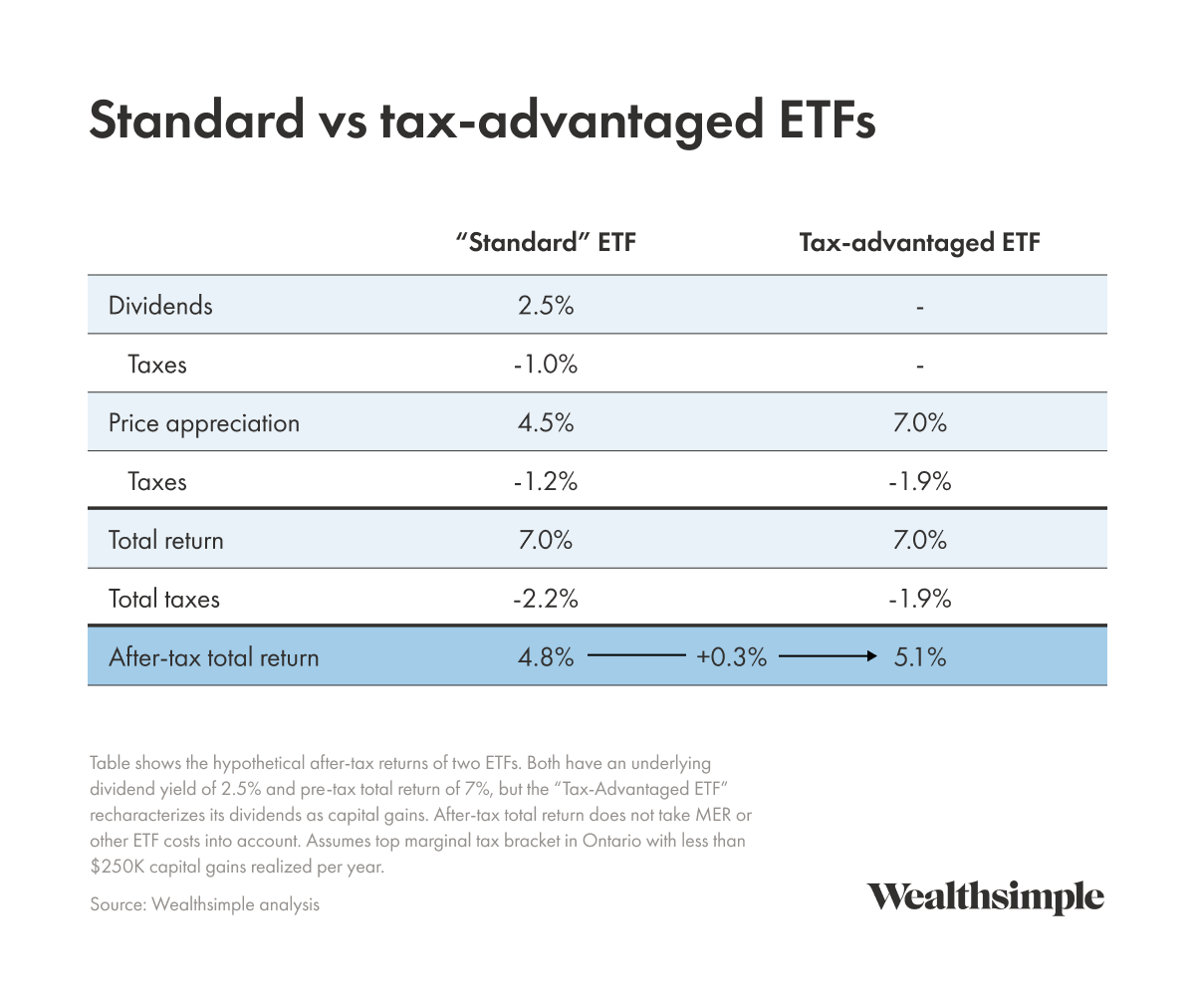

Tax-efficient ETFs and fund structures

Some Exchange-Traded Funds (ETFs) are structured to be more tax-efficient than others. Certain ETFs use "corporate class" or "swap-based" structures that can convert dividends into capital gains, which are taxed at a lower rate. Choosing these types of ETFs can improve your after-tax total returns, sometimes more than selecting a fund with a lower Management Expense Ratio (MER).

Asset location: which investments to hold where

Asset location is the practice of placing investments in the account type where they will be taxed most favourably. While asset allocation determines what you invest in, asset location determines where you hold those investments.

A general framework for asset location in Canada:

TFSA: Hold investments with the highest expected growth — such as equities and equity ETFs — since all gains and income are completely tax-free on withdrawal.

RRSP: Hold investments that generate interest income or foreign dividends, since these are taxed at the highest rates in non-registered accounts. U.S. dividend-paying stocks benefit from RRSP holding due to the Canada-U.S. tax treaty.

Non-registered account: Hold Canadian dividend-paying stocks to take advantage of the dividend tax credit. Capital gains-generating investments also work well here, since only a portion of capital gains is taxable.

The right asset location strategy depends on your personal tax situation, contribution room, and investment goals.

Most tax-efficient investments in canada

Not all investments are taxed equally. From most to least tax-efficient:

Capital gains-generating investments — Only a portion is included in taxable income.

Eligible Canadian dividends — Benefit from the dividend tax credit, which reduces the effective tax rate.

Non-eligible dividends — Receive a smaller dividend tax credit than eligible dividends.

Interest-bearing investments — Fully taxable at your marginal tax rate.

Knowing where each investment falls on this spectrum can help you make more informed decisions about what to hold and where.

Making tax-efficient investing work for you

Tax-efficient investing does not need to be complicated. Start by understanding how your investment income is taxed, then think carefully about which accounts to use for each type of investment.

Small decisions — like holding interest-bearing investments inside a registered account or choosing tax-efficient ETF structures — can meaningfully improve your after-tax returns over time. Every dollar saved on taxes is a dollar that stays invested and continues to grow.