There's often a difference — sometimes a big difference — between the mortgage that you qualify for and the mortgage you can actually afford. The bank's number is usually going to be higher.

That's not because banks are out to get you. They just don't know you, especially in the preapproval phase. They have no idea whether you're naturally frugal or more likely to spend on big discretionary purchases.

But you do. And this is not the moment to delude yourself. In this article, we'll walk through how to figure out what you can actually afford each month, how lenders calculate your borrowing limit, and how to make sure the two numbers don't leave you under financial pressure.

How much you can afford each month

A common rule of thumb is to spend no more than 28% to 35% of your gross monthly income on housing costs, including your mortgage payment, property taxes, heating, and insurance. Affordability isn't about the maximum amount a bank will lend you — it's about how much you can comfortably part with every 30 days without feeling strained.

Your mortgage payment will be your biggest recurring expense, so it needs to fit into your life alongside groceries, utilities, and the occasional night out.

How you can get a figure that's more appropriate for your budget

Determine how much you're comfortable paying your mortgage lender each month without squeezing your day-to-day spending. Build in breathing room for surprises. In other words, start with a detailed budget.

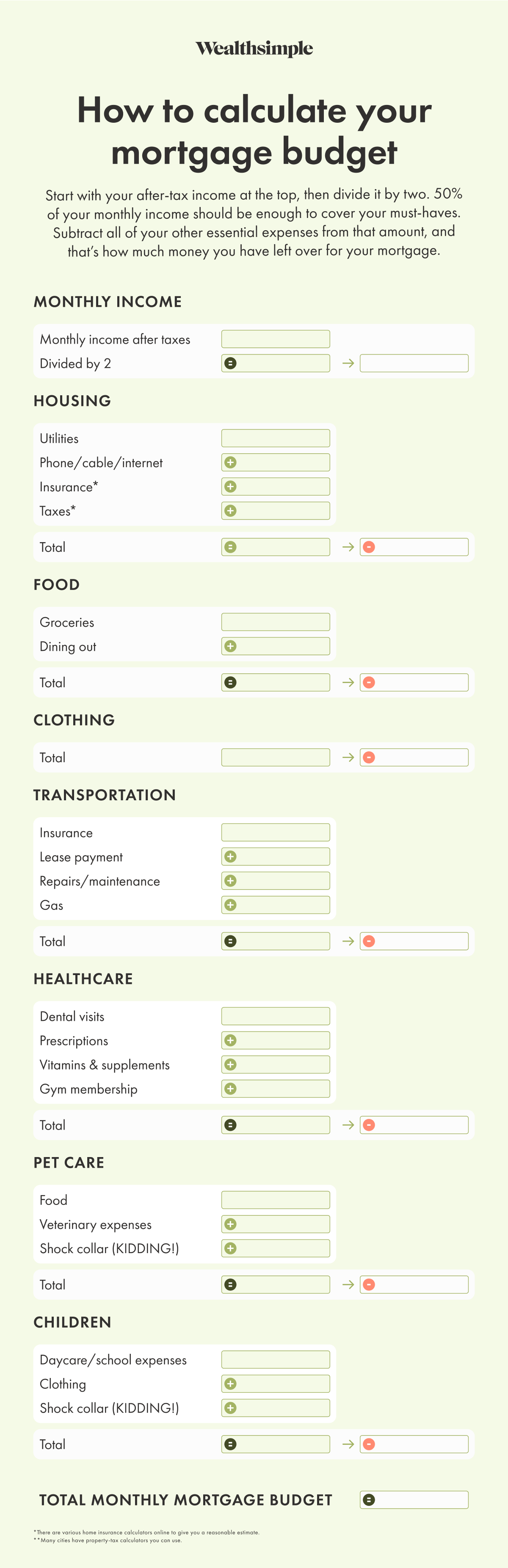

One classic budgeting approach is the 50/30/20 rule for your after-tax income:

50% for needs: food, utilities, clothing, and housing costs (such as your mortgage).

30% for wants: holidays, subscriptions, and dining out.

20% for debt and savings: student loans, credit cards, and an emergency fund.

Since the "needs" column is what your future mortgage will go under, you can focus on only that part to help minimize the math. Here's a template to help you figure things out.

Once you have your optimal mortgage payment, experts recommend lowering that number by at least 5% to give yourself wiggle room in the event of a spike in interest rates.

It's called "payment shock." Depending on the size of your loan and whether you have a fixed or variable rate, a rate change from the central bank can add several hundred dollars to your monthly payment.

You may also want to add extra cushion in case your income decreases (for example, due to job loss) or your expenses increase (for example, after a change in family circumstances). And don't forget closing costs (land transfer tax can be a significant expense) and any possible renovations you might want to make.

Those are one-time fees, but if you've forgotten to consider them and your down payment wipes out your savings, you can't actually afford the home. (If you're a first-time buyer, the Home Buyers' Plan may help with your down payment.) To find out what kind of mortgage that payment will cover, you can pull up a home affordability calculator online, or use this template:

How lenders decide what you qualify for

Banks base their pre-approval on what's known as the five C's:

Capital: how much money you can put toward a down payment

Collateral: the value of the home you are borrowing against. When it's time to turn your pre-approval into actual approval, the bank requires an appraisal to make sure the home you're buying is actually worth it.

Character: your job history and job security, along with your track record when it comes to paying back past debts

Capacity: how much income you have coming in to help you pay your mortgage each month, also known as your Total Debt Service Ratio (TDS)

Conditions: everything from the interest rate of the loan to the state of the economy

Your credit score doesn't factor in nearly as much as you might imagine: as long as it's above 650, you won't get dinged. Anything below 650, however, results in a higher interest rate and, if you need it, more costly mortgage insurance.

The Canadian mortgage stress test and debt ratios

When you apply for a mortgage, lenders look at two main debt ratios: the gross debt service (GDS) ratio and the total debt service (TDS) ratio.

Gross debt service (GDS) ratio: the percentage of your pre-tax income needed for housing costs (mortgage, property taxes, heating, and half of condo fees), with a maximum of 39%.

Total debt service (TDS) ratio: your housing costs plus all other debt obligations (car payments, student loans, and credit cards), with a maximum of 44%.

Go above those thresholds, and you'll have a harder time getting approved — or you may need to look at a smaller mortgage.

Then there's the mortgage stress test (MST). The federal government requires lenders to prove you could still afford your payments if interest rates went up.

For the MST, they'll calculate your ratios using a qualifying rate that's higher than the actual rate you're being offered — typically the greater of 5.25% or your contract rate plus 2%. It's basically a financial safety net to make sure you won't lose your home if rates climb.

Costs that change your real housing budget

Your mortgage payment is only one piece of the housing puzzle. When lenders calculate your affordability, they factor in property taxes, heating costs, and half of your condo fees if you're buying an apartment or townhouse.

But as a homeowner, you know the real list is longer. You have to account for home insurance, regular maintenance, utility bills, and the inevitable emergency repairs. A general rule of thumb is to set aside 1% to 3% of your home's value each year for upkeep.

Don't forget the upfront costs beyond your down payment:

Legal fees

Title insurance

Home inspection

Moving expenses

Land transfer tax, which can be tens of thousands of dollars in some provinces

Pre-qualification vs. pre-approval

These two terms sound nearly identical, but they serve very different purposes:

Pre-Qualification | Pre-Approval | |

|---|---|---|

| What it is | Quick estimate based on self-reported numbers | Verified assessment with credit check and income verification |

| Binding | Not a guarantee | Rate hold for 90–120 days |

| Best for | Getting a sense of your price range | Making serious offers on homes |

When you're ready to make an offer, you want a pre-approval in hand. Sellers take pre-approved buyers more seriously, and it speeds up the process once you've found the right place.

How to sanity-check your number before you buy

Once you have a target monthly payment in mind, take it for a test drive. If your estimated mortgage, taxes, and maintenance will cost $2,500 a month, and you currently pay $1,800 in rent, start putting that extra $700 into a savings account every month.

Do this for a few months before you buy. If things feel too tight, your target number is too high. If you manage it easily, you'll have extra cash for your down payment or moving expenses.

Next steps before you start house hunting

If you've run the numbers and feel confident about what you can afford, it's time to get your paperwork in order:

Recent pay stubs

Notices of assessment from the Canada Revenue Agency

Proof of your down payment

If self-employed: 2 years of tax returns and financial statements

Then, reach out to a mortgage broker or lender to start the pre-approval process. Having that official document will show sellers you're a serious buyer when you finally find the right place.

And remember: the number they give you is a ceiling, not a target. You're allowed — encouraged, even — to spend less.