Investing isn't something you set up once and leave until you're ready to retire. After all, most people probably wouldn't watch the same TV shows in their 20s as they do in their 40s and 50s (unless we're talking about Bluey!). It's similar to investing. How you use your money right out of university can look very different from how you manage it when you're watching your youngest child walk across the graduation stage.

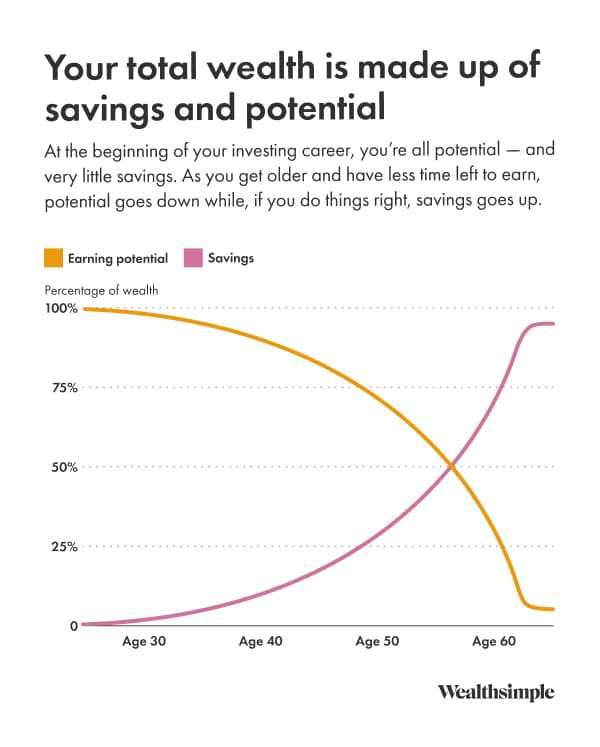

Wealth, at any point in time, is the sum of your savings (financial capital) and the money you make from working (human capital). When you're young, most people have little financial capital and a great deal of human capital. As you get older, your human capital gets converted to financial capital through saving and investing.

The key is knowing where you are on that path and how it affects your financial priorities and ability to take risks. Below, we'll cover the fundamentals that apply to everyone — what to invest in, which accounts to use, and how to think about fees and taxes — then get into how you might adjust your investing perspective based on your age.

Why investing matters at any age

Investing helps you build wealth by growing your money faster than inflation and generating compound returns over time. You work hard for your money — investing is how you get your money to return the favour.

While saving is great for short-term goals, keeping all your cash in a standard chequing account means you could be losing purchasing power over time. If inflation is running at 3% and your savings aren’t earning that much, your buying power is shrinking every year.

Investing helps you outpace inflation, but a key advantage is compound growth — when the money you earn on your investments starts earning money itself. The earlier you start, the sooner you'll reach your savings goals.

Here's an example of what compound growth could look like:

Start at 25: Invest $200 per month until age 65 and earn 7% annually (hypothetically) to reach roughly $525,000.

Start at 35: Invest $200 per month until age 65 and earn 7% annually (hypothetically) to reach roughly $245,000.

In this example, starting 10 years later results in about $280,000 less by age 65. Starting earlier can make compounding work more in your favour (though actual returns can vary).

Before you invest, do these five things

It's tempting to jump straight into the stock market, but a little prep work can prevent a lot of headaches (and panic) later. Here's a quick checklist to tackle first:

Pay off high-interest debt. If you have credit card debt charging you 20% interest, paying that off is a guaranteed 20% saving. Market returns are not guaranteed.

Build an emergency fund. Aim for having 3 to 6 months of your household income in a high-interest savings account. This prevents you from having to sell your investments because the car broke down or the furnace gave up.

Define your goals. Are you buying a house in 3 years or retiring in 30? Your timeline dictates what you should buy and how much risk you can reasonably take.

Understand your risk tolerance. How much volatility can you stomach? If seeing your portfolio drop 10% in a week would make you lose sleep, you likely need a more conservative portfolio.

Pick a strategy. Decide if you want to pick stocks yourself (DIY) or use a managed service that does the heavy lifting for you.

What you can invest in (in plain English)

The investment world is full of jargon, but most portfolios are built upon a few key asset types:

Stocks (equities): When you buy a stock, you're buying a tiny piece of ownership in a company. They tend to offer higher growth potential but come with higher risk.

Bonds (fixed income): This is essentially lending money to a government or company for a set period in exchange for interest payments. They're generally safer than stocks and help smooth out the ride.

Exchange-traded funds (ETFs): An ETF is a basket of stocks or bonds that trades on an exchange like a single stock. Instead of trying to pick the one winner, you buy the whole basket. It's an easy, low-cost way to get instant diversification.

Guaranteed Investment Certificates (GICs): You lend money to a bank for a fixed term, and they guarantee your principal plus a set interest rate. It is generally considered low risk, but your money is typically locked in for the term.

Mutual funds: Like ETFs, these are pooled funds managed by professionals. However, they often come with higher fees and minimum investment requirements compared to ETFs.

Choosing accounts in Canada: TFSA, RRSP, and FHSA

In Canada, where you hold your investments is as important as what you invest in. Using the right registered account can save you a bundle in taxes.

Tax-Free Savings Account (TFSA): Don't let the name fool you — it's not for savings only. You can hold investments in it, and any growth or withdrawals are completely tax-free. It's flexible and great for both short- and long-term goals.

Registered Retirement Savings Plan (RRSP): Contributions reduce your taxable income today, which may lead to a nice tax refund. You pay tax when you withdraw the money, ideally in retirement when your income (and tax rate) is lower.

First Home Savings Account (FHSA): The new kid on the block. It combines the features of both RRSPs and TFSAs for aspiring homeowners: contributions are tax-deductible (like an RRSP) and withdrawals for a qualifying home purchase are tax-free (like a TFSA).

Non-registered (personal) account: If you've maxed out your registered accounts, this is a standard investment account. You don't get tax breaks, and you'll have to pay tax on capital gains and dividends.

Fees and taxes to understand before you start

Fees can reduce your net returns over time, especially when they compound across many years. The most common one to watch is the management expense ratio (MER), the annual fee charged by mutual funds and ETFs to cover operating costs.

Investment type | Typical MER* | $10,000 over 20 years |

|---|---|---|

| Mutual Fund | 2% | ~$24,300 |

| ETF | 0.2% | ~$29,200 |

*2% is the average cost of equity mutual funds in Canada. Actual fees may vary.

That difference might sound small, but it can mean nearly $5,000 staying in your pocket instead of going to a fund manager. You can use a fee calculator to see how fees affect your own investments.

You should also be aware of trading commissions (the fee to buy or sell a stock) and foreign exchange fees if you're buying U.S. assets. And don't forget the taxman: unless your money is in a TFSA or FHSA, you will have to pay taxes on the money your investments make when you withdraw them.

How to invest in your 20s

Your twenties are an exciting time, full of possibilities and new adventures — like your first solo trip to Paris or setting up your own dentist appointment without a parent's help. When it comes to your finances, start with the five steps above (especially paying off high-interest debt and building an emergency fund). After that, the next priorities are:

Maximize employer contribution matching if available. Contribute enough to an eligible savings plan (typically a group plan) to receive the full available employer match if your plan offers one. That can meaningfully increase your total compensation and overall savings.

Automate contributions. Set up an automatic transfer to a secondary savings or registered account to build the habit. If you can afford to put aside 20% of your paycheque each month, do it.

Choose a simple diversified portfolio. Some young investors don't know how to start and can be paralyzed by the options. We usually recommend investing in a low-cost, diversified portfolio, preferably in a tax-advantaged account.

How to invest in your 30s and early 40s

The average person will see their income roughly double between age 25 to 40. You may start to have some real savings at this point, but with that higher salary, your most significant asset is still human capital.

This period often comes with higher costs, such as buying a home or starting a family. It's also when smart people protect their human capital by purchasing life and disability insurance — if you were unable to work due to illness or an injury, your income could decrease significantly, which can be difficult for anyone who depends on it.

Despite the new strains on your finances, saving with discipline is still very important. Here's what to prioritize:

Prioritize RRSP contributions: As your pay increases, your marginal tax rate may rise, which can make RRSP deductions more valuable.

Consider an appropriate level of risk: Your capacity for investment risk is often higher at this stage, even if volatility feels uncomfortable.

Keep perspective: A percentage loss may be smaller in context when compared with future earnings and years of saving ahead.

How to invest in your late 40s and 50s

The 40s and 50s are peak earning years for most people. But they come with more pressure (and reading glasses). With retirement on the horizon, this is a good time to start defining your retirement goals more precisely.

By now, you've accumulated enough wealth that how you invest and how much risk you take can have significant consequences. It can help to think about the full range of outcomes your investments could experience, not just the most likely scenario. With fewer years of saving remaining, it becomes more challenging to make up for poor results.

With this in mind, many investors begin reducing their exposure to equities. But keep things in perspective: you could still have 20 years to go until retirement. That's a relatively long timeline, and the chances of experiencing significant losses in a high-risk portfolio over that period are extremely low.

Everyone is unique, and your approach should be informed by how on track you are for your retirement goals:

If you are ahead of target: You may be able to take on more risk, because your needs may still be met even if returns are lower than expected.

If you are behind target: Consider reducing risk to limit the chance of a large shortfall, even if that means adjusting your goal or timeline.

One more thing to consider: if the interest rate on your mortgage is higher than what you expect to make (after taxes) by investing in a non-registered account, you may want to think about putting extra savings toward your mortgage. Reducing a negative return like mortgage interest is as good as generating a positive one.

How to invest in your 60s and beyond

By your 60s and 70s, most investors are often partially or fully retired with considerably less employment income. You have a much lower ability to offset material financial setbacks at this point, so it can be smart to reduce investment risk by increasing your allocation to bonds and cash equivalents.

Not that you should give up on risk entirely. If things go your way, you still have decades left. A little risk can help you keep your savings growing, counter the effects of inflation, and limit the chances of running out of money too soon.

Now can also be a good time to think about permanent life insurance. (Term insurance, at this point, becomes less important, since your human capital is winding down.) These plans cost more than term insurance, but they can provide a guaranteed benefit to your beneficiaries.

And finally, it's important to maximize the wealth you've so diligently saved. You can do that in two ways:

Taking government pensions at the right time. A lot of Canadians take their benefits as soon as possible, which isn't usually the most effective strategy. You can take a reduced Canada Pension Plan (CPP) or Quebec Pension Plan (QPP) benefit as early as age 60, or defer CPP or QPP and Old Age Security (OAS) as late as age 70 to receive more each month.

Withdrawing from the right accounts — in the right order. Although you can't avoid taxes in retirement, you can influence how much you are taxed. Rather than waiting until you turn 72, when you generally must start withdrawing from a Registered Retirement Income Fund (RRIF) (or converting your RRSP to a RRIF), many people may benefit from starting withdrawals earlier to smooth taxable income. It can get complicated, so we'd suggest catching up with an advisor or a financial planner.

Your next steps if you want to start now

Ready to get going? You generally have two paths:

Do-it-yourself (DIY) investing: Open a trading account and buy stocks or exchange-traded funds (ETFs) if you want hands-on control.

Managed investing: Use a managed portfolio service (often offered by a digital adviser) that builds a diversified portfolio based on your goals and risk tolerance.

Whichever path you choose, the most important step is the first one.