Regardless of where you invest your money, you're essentially giving it to a company, government, or other entity in the hope that they provide you with more money in the future. People generally invest money with a specific goal in mind — retirement, their children's education, a house, and so on. This guide covers the key concepts and steps to help you get started: what investing actually is, how to tell if you're ready, the steps to take your first action, and the accounts and costs you should understand along the way.

What investing is and what it isn't

Investing means putting money into assets—such as stocks, bonds, or real estate—with the expectation that they may grow in value over time. It can involve buying shares of a company, lending money to earn interest, or purchasing property with the goal of earning a return.

Here's how investing differs from the alternatives:

Saving: Put money in a safe, accessible place (such as a bank account) for short-term needs, with lower risk and lower growth potential.

Trading: Buy and sell assets frequently to try to profit from short-term price changes; it can require significant time and expertise and can involve higher risk.

Investing: Put money into assets for the long term, accepting some risk in exchange for the potential for growth over years or decades.

Things to consider before you invest

Before you start investing, make sure you're financially ready by asking yourself two critical questions:

Do you have high-interest debt? It's often difficult for investments to reliably outpace high-interest credit card debt (which can be around 20% or more, depending on the card). Consider paying it down first before investing.

Do you have an emergency fund? You should have six months to one year of living expenses in cash or a savings account. If you don't have this cushion yet, consider building it before you invest.

How to start investing in 5 steps

Getting started can feel overwhelming, but it's much easier when you break it down into a few simple steps.

Set your goals. Figure out what you're investing for (for example, retirement, a down payment on a house, or a child's education).

Choose an account type. Decide where your investments will be held (for example, a registered account with potential tax advantages).

Pick investments. Choose individual stocks and bonds, or consider diversified funds such as exchange-traded funds (ETFs) or mutual funds.

Choose an approach. Either manage your own portfolio (do it yourself) or use an automated service (such as a robo-advisor).

Automate contributions. Set up a recurring transfer from your chequing account to your investment account.

Investing tips for beginners

Before we go over the specifics of what you can consider investing in — stocks, bonds, or your cousin Brian's yak farm — let's first go over the basics of how one invests.

For many people, investing starts when there's money left at the end of the month to put toward future goals. In practice, it usually requires setting money aside regularly. How are you supposed to find those elusive extra dollars to save? Here's how.

Avoid lifestyle creep

In all likelihood, you'll earn more in your thirties than you did in your twenties, and even more than that in your forties. The key to saving is to do your absolute best to avoid what's called "lifestyle creep." Lifestyle creep means that as you make more money, what once seemed like luxuries become necessities.

A pricey tasting menu might be tempting, but having $600 available doesn't necessarily mean it's the right choice for your goals. Instead, do your best to live the same way you've always lived. Skip the pigeon, get yourself a croque monsieur, and invest the 600 bucks you saved.

Start investing — even a little at a time

Investing is not just for people like Warren Buffett. Anyone can start with small, regular contributions. If you're finding it tough to put away some investing money each month, try using a spare change app. These services round up your purchases, allowing you to invest small amounts of money that you'd hardly miss.

Investing small amounts is a helpful habit, and those contributions can add up over time. Here are some other easy ways to invest with a little money:

Set up small monthly transfers from your chequing account.

Use a low-cost investing service.

Build a budget.

Consider investing any tax refunds.

Consider investing some or all of any raises to avoid lifestyle creep.

If it suits your situation, ask for cash gifts that you can put toward your investments.

Know what you're investing for

How you invest depends on what you're investing for. You might be investing money to help your teenager with her upcoming university tuition, or you might want to invest money to live off when you retire in 30 years. The "time horizon," or the point at which you need your money, for each of these investments is very different.

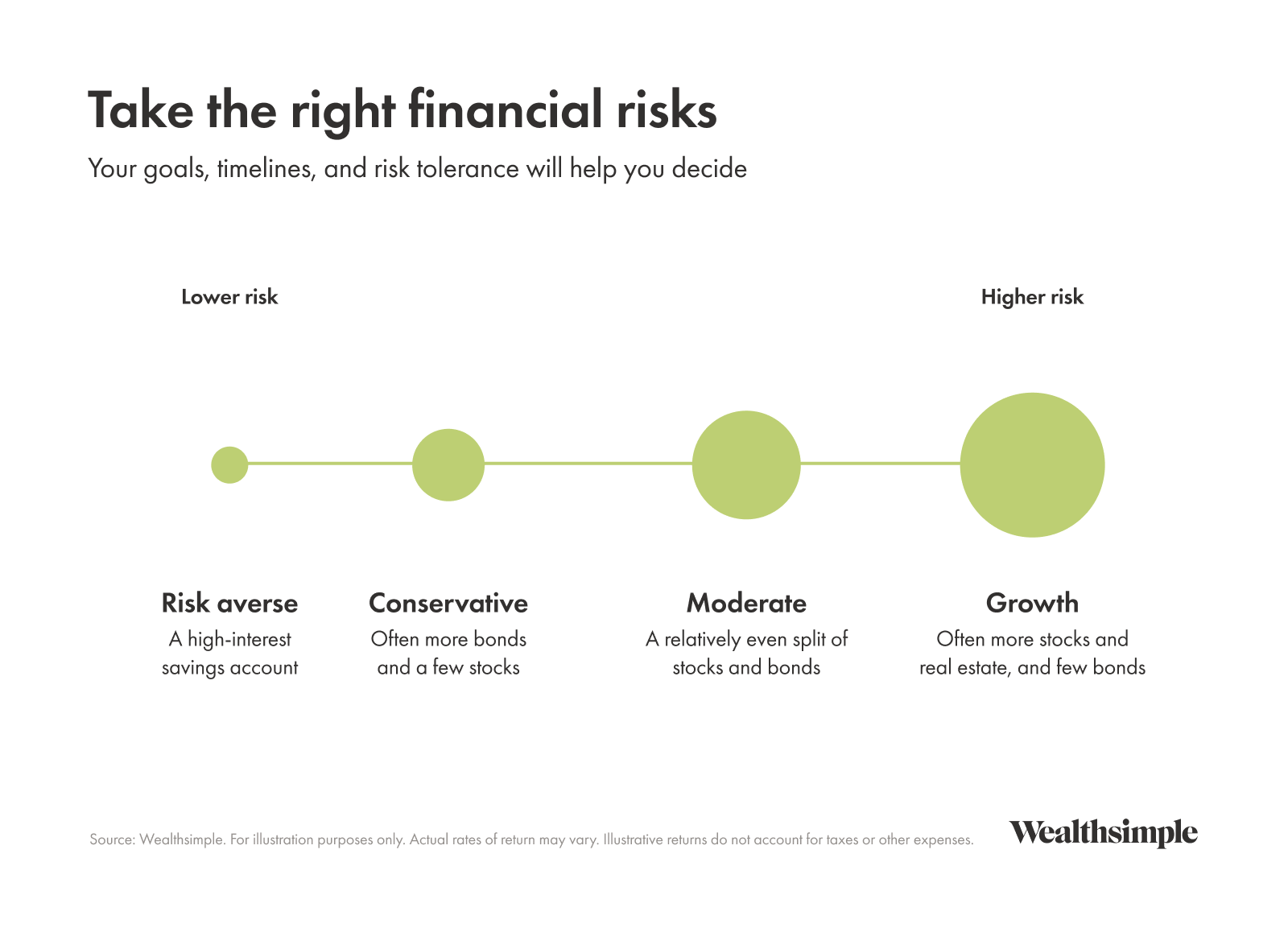

With a shorter time horizon, a more conservative approach is often appropriate. With a longer horizon, you may be able to take on more risk.

Understand the risk you are taking

Good investors know their risk tolerance. In other words, it's how much fluctuation or loss you can realistically handle. If you may need the money soon—for example, for next month's rent—taking on investment risk may not be appropriate right now.

If losing some or all of an investment would not significantly affect your day-to-day finances, you may be able to tolerate more risk. Risk tolerance is often dictated by your time horizon.

Diversify your investments

Instead of relying on a single stock, spread your money across different holdings. Diversification can include multiple geographies, industries, and asset classes (such as stocks, bonds, and real estate).

Fluctuations aren't necessarily the biggest risk for investors in it for the long haul. A potentially bigger risk is how you react to those fluctuations. Many investors find it difficult to stick to their investing plan, particularly during market movements.

If certain stocks are outperforming other assets, for example, it can be easy to think you should add more of those stocks to your portfolio. But then when stocks fall, you're going to take a much larger hit than you would have had you stuck to your original plan. A diversified portfolio is a great tool to help manage your emotions and maintain your investment plan.

Invest for the long term

Many studies suggest that, historically, holding stocks over long periods (such as 10+ years) has increased the likelihood of higher returns, though outcomes are never guaranteed. That's not to say this trend will continue, or that risk is ever totally eliminated. Risk never disappears, but you might say it mellows with age.

If you can put money away for a long time, then you can afford to have investments that are typically more susceptible to rising and falling. Your portfolio can contain a mix of stocks and equities, which are typically more volatile compared to bonds.

Another big benefit of investing for a long time period is thepower of compounding. This is the process by which the money you make earns interest on itself over time. The earlier you start investing, the more compounding you get.

Watch out for high fees

Investing involves fees; you can't control that. But you can control how high your fees get. Higher fees cause a significant drag on your returns. Depending on your return assumptions, time horizon, and fee level, paying 1–2% in fees could reduce your ending balance substantially over time.

Here's how fees impact gains on a $10,000 initial investment with a $300 monthly contribution for 30 years (assuming a return of 5.48%).

Investment type | Average mutual fund (2.08% fee) | Automated investing (0.5% fee) |

|---|---|---|

| Starting amount | $10,000 | $10,000 |

| Year 10 | $56,311 | $62,508 |

| Year 20 | $120,471 | $147,851 |

| Year 30 | $209,265 | $286,563 |

Source: Wealthsimple. For illustration purposes only. Actual rates of return may vary. Illustrative returns do not account for taxes and other expenses.

It can be well worth paying a fee for a professionally designed investment portfolio that can be adjusted as your life changes. It's also handy to have features like automatic rebalancing, which ensures that your portfolio always contains the correct mix of assets.

Make an investing plan and stick to it

One of the biggest reasons many investors have low returns is because they sell at the wrong time. They often base decisions on recent performance. Many investors tend to buy things that have appreciated in value and sell things that have declined in value.

Create a plan you believe you can follow over your timeline, and avoid making changes based primarily on short-term market moves or recent performance.

Types of investment

Understanding the main types of investments helps you build a diversified portfolio. Here are the most common options for beginners:

Investment | What it is | How to invest |

|---|---|---|

| Bonds | A loan (kind of like an IOU) with interest. They are often issued by governments. Bond yields may be higher than rates on some savings accounts, but returns and risk vary by issuer and bond type. | They can be purchased directly through the government, a brokerage, or trading platform. They are often included in managed portfolios, too. |

| Stocks | A tiny piece of a company that anyone can buy. Stocks are volatile, and while you could make a lot, you could also lose a lot. When you pick individual stocks, you lack diversification. | Through a broker or automated investing platform. Stocks are often a large part of managed portfolios. |

| Real estate | Purchasing real estate such as apartments or houses. There can be a high barrier to entry, as property is expensive. Real Estate Investment Trusts (REITs) can let you invest in a small share of a diversified real estate portfolio. | Directly from a property owner. REITs can be purchased through a broker. Managed investment portfolios often contain some real estate. |

Investment accounts you can use in Canada

When you invest in Canada, you have access to special registered accounts designed to help you save on taxes. Think of these accounts as baskets; you can hold various investments like stocks, bonds, and ETFs inside them.

Account type | Best for | Tax benefit | Key feature |

|---|---|---|---|

| TFSA | Flexible goals, any timeline | Tax-free growth and withdrawals | No tax deduction going in, no tax coming out |

| RRSP | Retirement savings | Tax deduction on contributions | Contributions lower your taxable income; pay tax on withdrawals |

| FHSA | First home purchase | Tax deduction + tax-free withdrawal | Combines TFSA and RRSP benefits for home buyers |

| RESP | Child's education | Government grants | Government adds money to your contributions |

Costs and taxes to consider

Every dollar you pay in fees or taxes is a dollar that's not growing in your portfolio. While you can't avoid them entirely, understanding them helps you keep more of your money.

Management fees

If you buy a mutual fund or an ETF, or if you use an automated investing service, you will pay a fee for the management of those assets. This is often expressed as a management expense ratio (MER). A lower MER means you keep more of your returns.

Trading commissions

Some brokerages charge a flat fee every time you buy or sell an investment. If you're investing small amounts regularly, these fees can eat into your savings quickly. Look for platforms that offer low or zero-commission trading.

Taxes on investments

If you invest outside of a registered account (like a TFSA or RRSP), you will have to pay taxes on the money your investments make. This includes taxes on interest, dividends, and capital gains (the profit you make when you sell an investment for more than you paid for it). Using registered accounts effectively is the standard way to minimise your tax bill.

What to do in the next 30 days

Reading about investing is great, but taking action is what actually builds wealth. Here's a simple checklist to help you get started over the next month.

Week 1: Check your financial foundation. Make sure you have a plan for high-interest debt and have started building an emergency fund.

Week 2: Define your first investing goal. Write down what you're saving for and when you'll need the money.

Week 3: Open an account. Decide whether a TFSA, RRSP, or another account fits your goal, and then open the account.

Week 4: Set up an automatic transfer. Pick an amount you're comfortable with (even $25 a week) and schedule it to transfer automatically to your investment account.

Once you've taken these steps, you've completed an important first step. Next, focus on staying consistent and giving your plan time to work.

Frequently asked questions (FAQs) about investing for beginners

How should beginners start investing?

Start by confirming your financial foundation (high-interest debt and an emergency fund), then open a registered account and consider a diversified investment option such as an all-in-one ETF. Automate contributions to build the habit.

Is investing $100 a week enough?

Yes. $100 (or even $25) a week can make a meaningful difference over time, especially if you contribute consistently and reinvest returns.

How much should I have invested before I expect income?

Generating meaningful income (like $1,000 a month) typically requires hundreds of thousands of dollars invested. Beginners should focus on growing their portfolio's total value rather than generating immediate income.

What is a reasonable return to expect over 10 years?

While past performance doesn't guarantee future results, diversified portfolios have historically grown steadily over the long term and outpaced inflation, though individual years will vary.

How do I avoid panic selling when markets drop?

Only invest money you won't need for several years, automate your contributions, and check your portfolio less frequently. Selling during downturns can realize losses and reduce the benefit of a later rebound, while staying invested may give your portfolio time to recover.