Your employer just told you about the company's group RRSP, and now you're being asked how much you should be contributing through payroll deductions. Fair enough — payroll deductions for retirement savings can feel abstract until you understand what's actually happening to your money.

A group Registered Retirement Savings Plan (GRRSP) works like a personal RRSP, except your contributions come straight off your paycheque before tax is calculated. That means you get your tax break immediately, not months later when you file your return. We'll walk through exactly how the deductions work, what employer matching looks like, and what happens to your money if you change jobs.

What is a group RRSP

A GRRSP is a retirement savings plan your employer sets up on behalf of employees. Contributions come straight from your paycheque (before you ever see the money) and go into an account registered in your name. The tax treatment works exactly like a personal RRSP: contributions are tax deductible and your investments grow tax-sheltered until you withdraw them.

You might hear it called a group RSP or GRRSP, depending on who's talking. Whatever the name, the defining features are the same:

Employer-sponsored: your company arranges the plan with a financial institution

Payroll-linked: contributions are automatically deducted from your gross pay

Tax-deductible: your contributions reduce your taxable income

Tax-sheltered: investment growth isn't taxed until withdrawal

Some employers also contribute on top of what you put in — essentially extra money toward your retirement.

Not every employer decides to chip in though, so it's worth asking your employer what your specific plan offers.

How group RRSP payroll deductions work

Here's the basic flow: you pick a contribution amount, your employer's payroll system deducts it from your gross pay each pay period, and the money gets sent to the plan provider. From there, it's invested according to whatever funds you've selected. Once you're enrolled, the whole thing runs on autopilot.

The key difference between a group RRSP and contributing to your own personal RRSP comes down to timing — specifically, when you get your tax break.

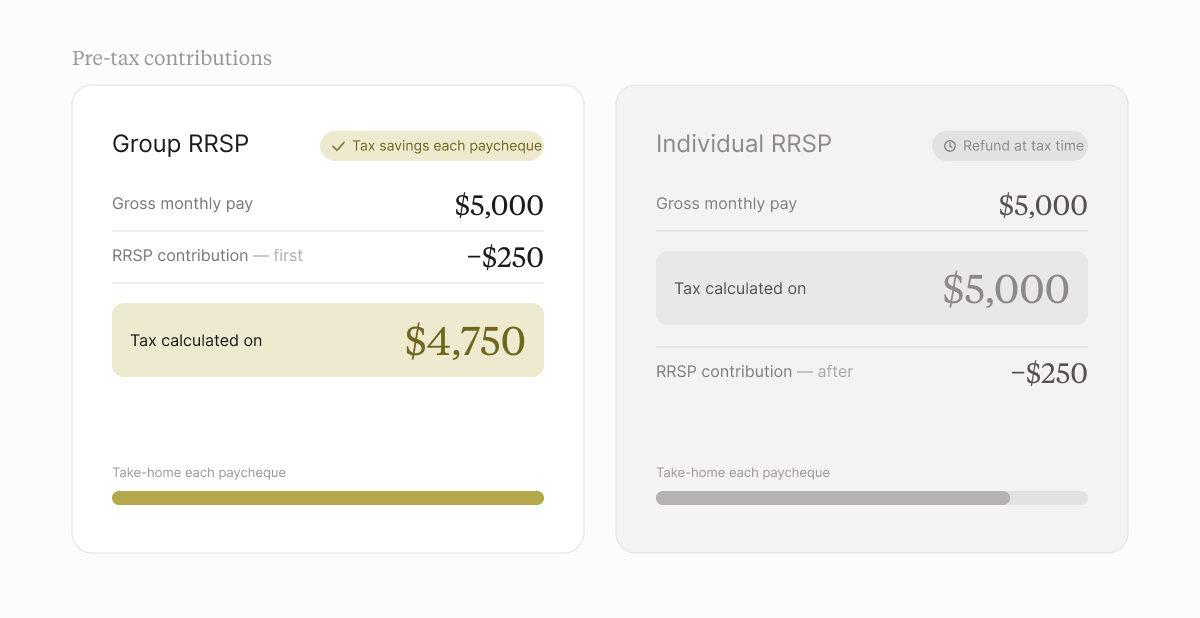

Pre-tax contributions and instant tax savings

With group RRSPs, your employer deducts contributions before calculating income tax on your paycheque. That means you pay less tax right away, not months later when you file your return.

Compare that to contributing to a personal RRSP on your own. In that case, you pay tax on your full paycheque first, make your contribution with after-tax dollars, then wait until tax season to claim the deduction and get a refund. With a group RRSP, you skip the waiting.

Here's a quick example: say you earn $5,000 per month and contribute $250 to your group RRSP. Income tax gets calculated on $4,750, not $5,000. Your take-home pay ends up higher on every paycheque compared to making the same contribution post-tax and waiting for a refund. Same contribution, different timing – and a bigger pay cheque.

Same contribution amount, different timing — and a bigger paycheque.

How your contribution amount gets calculated

When you enrol, you'll typically set your contribution as either a percentage of your gross salary or a fixed dollar amount per pay period — though which options are available depends on your plan rules. Some plans let you pick either, while others only support one method. The payroll system handles the math from there.

Choosing a percentage means your contributions automatically go up when you get a raise. A fixed amount stays the same until you change it. Most plans let you adjust your contribution rate a few times per year, though the exact rules vary by employer.

When contributions hit your account

Contributions are usually sent to the plan provider within a few business days of each paycheque. Once the money arrives, it gets invested according to your investment selections.

Most plan providers offer an online portal or app where you can track your contribution history and account balance.

How employer RRSP matching programs work

Many employers add their own money to your group RRSP on top of what you contribute — part of your total compensation. This usually takes one of two forms:

Matching contributions: the employer contributes based on how much you put in, so you only receive it if you contribute. This is the most common structure and is often described as "free money," which isn't far off.

Base contributions: the employer contributes a set amount regardless of whether you contribute anything yourself — for example, a flat percentage of your salary that everyone receives.

Some plans combine the two: a base contribution everyone gets, plus matching on top if you contribute. Not every group RRSP includes employer contributions at all, though, so it's worth confirming what your specific plan offers.

Common employer matching formulas

When a plan does include matching, the formula determines how much you'll want to contribute to capture the full benefit. Most matching structures fall into one of three categories:

Dollar-for-dollar match: your employer contributes the same amount you do, up to a cap

Partial match: your employer contributes a fraction of what you put in, like 50 cents for every dollar

Tiered match: the matching percentage increases with your years of service

Employers often cap matching at a percentage of your salary. Contributions above that threshold don't receive any additional match.

How to maximize your employer contribution

The general rule: contribute at least enough to capture the full employer contribution. Anything less means you're leaving money on the table.

If your employer matches dollar-for-dollar up to 3% of your salary and you're contributing 1%, you're forfeiting 2% of your salary in free retirement savings. Ask HR for the exact contribution formula before setting your contribution rate.

Tax benefits of contributing through payroll

The tax mechanics are what make a group RRSP different from saving on your own — even if the contribution amounts are identical.

Lower taxable income on every paycheque

Because contributions are deducted pre-tax, each paycheque reflects a lower taxable income. Less income tax is withheld at source, and you don't have to wait until filing season to see the benefit.

This also means you're less likely to face a surprise tax bill when you file, since your withholding has been adjusted throughout the year.

Group RRSP contributions vs. individual RRSP contributions

Feature | Group RRSP (payroll) | Individual RRSP |

|---|---|---|

| Tax reduction timing | Each paycheque | Annual tax refund at filing |

| Contribution method | Automatic payroll deduction or manual contributions | Manual contribution |

| Contribution flexibility | Tied to payroll cycles | Tied to payroll cycles |

| Investment options | Curated selection set by the employer | Broad and selected by you — stocks, ETFs, GICs, etc. |

| Fees | Often lower investment management fees | Generally higher, varies by provider |

| Employer contribution | Permissible | Not permissible |

| Withdrawal restrictions | Plan sponsor may restrict withdrawals while employed | None — withdraw anytime, subject to tax |

The group RRSP wins on automation, tax timing, and potential employer contribution. The individual RRSP wins on flexibility and investment choice.

What shows up on your tax slips

Your contributions reduce the employment income reported on your T4, reflecting the pre-tax deduction. The plan administrator issues RRSP contribution receipts annually — typically two per tax year: one for March–December contributions and one for the first 60 days of the following calendar year.

Cross-reference your T4 with your CRA My Account to track your available contribution room.

How to set up your group RRSP contributions

The exact process varies by employer, but the general steps are consistent.

1. Enrol in your employer's plan

HR or the plan provider will supply enrolment forms — either paper-based or through an online portal. Some employers auto-enroll employees at a default contribution rate, while others require you to opt in.

Confirm the enrollment deadline and whether there's a waiting period before new employees are eligible.

2. Choose your contribution amount

The most important factor: contribute at least enough to capture the full employer match if one is offered. Beyond that threshold, consider your overall budget, other savings goals (TFSA, FHSA, mortgage), and your remaining RRSP contribution room.

Both your contributions and employer contributions count against your annual RRSP limit.

3. Select your investments

During enrollment, you'll choose how your contributions are invested from the available investment menu. Common options include equity funds, balanced funds, fixed-income funds, and target-date funds.

Target-date funds are a straightforward choice if you don't want to actively manage your portfolio. You select the fund closest to your expected retirement year, and the fund adjusts its allocation over time. Most providers offer a default fund if no investment selection is made, but everyone has different risk capacity, tolerance, and investment horizon, so it’s important to take the time to review and select investments that are suited for your needs.

4. Adjust your contributions when needed

Most plans allow you to change your contribution rate a limited number of times throughout the year. Common reasons to adjust include a salary increase, a change in financial circumstances, or approaching your annual RRSP contribution limit.

Changes typically take effect from the next payroll cycle after they're processed.

What happens to your group RRSP when you leave your job

The money in a group RRSP belongs to you (subject to vesting rules for employer contributions), not your employer. You have options when you leave.

Transferring to a personal RRSP

The most common approach is a direct transfer to a personal RRSP. A direct transfer doesn't trigger withholding tax and doesn't count as a withdrawal — the tax-sheltered status of your funds stays intact.

Moving to the provider's plan for former members

You can't stay in the employer's group plan once you leave, but your funds don't have to move institutions right away. By default, the provider transitions former employees into a separate plan for terminated members — and this is also what happens automatically if you don't respond to the options package you receive when you leave. Employer matching stops, but fees in these former-member plans are typically more competitive than a retail RRSP, even if not as low as the active group rate.

Withdraw your funds, less applicable taxes

Withdrawing cash from a group RRSP triggers mandatory withholding tax:

Up to $5,000: 10% withholding

$5,001–$15,000: 20% withholding

Over $15,000: 30% withholding

The withdrawn amount is also added to your taxable income for that year. Transferring rather than withdrawing avoids unnecessary tax consequences.

What happens to your group RRSP when you retire

Retiring is just a specific kind of leaving — your funds are still yours, but instead of continuing to save, you'll generally be looking to turn them into retirement income. Your main options are:

Convert to a RRIF: a Registered Retirement Income Fund is the most common path. You transfer your RRSP funds in directly (no tax on the transfer) and then draw a minimum amount each year, taxed as income as you withdraw it.

Purchase an annuity: you use the funds to buy a guaranteed stream of income for life or a set period. This trades flexibility for certainty.

A combination: many retirees use a RRIF for flexibility and an annuity for a guaranteed income floor.

You're also still free to transfer the funds to a personal RRSP first if you're not ready to start drawing income — RRSPs don't have to be converted until the end of the year you turn 71, at which point they must be moved to a RRIF or annuity.

Group RRSP contribution limits and deadlines

Both employee contributions and employer contributions count against your annual RRSP contribution limit. This is a common source of confusion.

How employer contributions affect your RRSP room

Your annual RRSP contribution limit is 18% of the previous year's earned income, up to the CRA's annual dollar maximum. Check your most recent Notice of Assessment (NOA) for your personal limit.

If you contribute $4,000 and your employer contributes $2,000, a total of $6,000 has been used from your contribution room. If you also contribute to a personal RRSP, you'll need to account for all contributions across all accounts to avoid over-contributing.

The annual RRSP contribution deadline

The RRSP contribution deadline is 60 days after December 31 of the tax year. Payroll contributions deducted in a calendar year are applied to that calendar year — they can't be retroactively applied to the previous tax year.

If you want to make additional contributions to reduce your tax bill for the prior year, do so before the deadline through your personal RRSP.

Group RRSP vs. pension plans

A group RRSP is not a pension plan, though the two are often confused.

Group RRSP: you own the account; both you and your employer can contribute; the employer promises a contribution (if any), not an outcome; investment risk is on you; portable; funds are not locked in

Defined contribution (DC) pension: like a group RRSP, both you and your employer contribute to an account in your name; the employer promises a set contribution amount, not a specific retirement income; investment risk is on you; but unlike a group RRSP, it's governed by pension legislation and funds are typically locked in until retirement

Defined benefit (DB) pension: the employer promises a specific monthly income in retirement; investment risk is on the employer; less portable

Neither a group RRSP nor a DC pension guarantees a specific retirement income — only a defined benefit pension does that. A group RRSP also isn't subject to pension legislation the way both pension types are.