News

We Built Our Portfolios to Protect Your Money In a Downturn. Here's Why it Worked

Our new portfolios outperformed our old portfolios (not to mention Canada’s largest mutual funds). Of course, no one should focus on short-term performance, but a look at why these changes worked will help you understand why not all diversification is created equal.

Wealthsimple makes powerful financial tools to help you grow and manage your money. Learn more

About nine months ago, we did some tinkering with our portfolios. The principles that underpin our investment strategy didn’t change — we don’t take bets based on what we think the market will do; instead, we believe the best results come from designing a mix of passive investments optimized for diversity and cost, tailored to the right risk level for each client and then...doing nothing. But we’re also humble enough to examine our strategy and see if there’s not a better way to do all that. Which is what we did last summer. You can read about what we did here. But for the TL;DR-ers out there, it basically boils down to adding longer-term bonds (which are more volatile, have higher returns on average, and perform better in downturns) and minimum volatility stocks (which tend to be more stable during wild swings in the market but otherwise have about equal performance to the equities they replaced, which were weighted according to market capitalization). The whole idea was to protect our clients by making our portfolios more resilient in a downturn.

Well, we’ve certainly had a downturn. Two months isn’t a huge sample size, and just like no one predicted the economic shockwaves the coronavirus has sent through the market so far, no one knows exactly what will happen next. But we wanted to give you a peek under the hood to see whether what we changed worked, and to explain why protection from market crashes is so important in the long term.

Sign up for our weekly non-boring newsletter about money, markets, and more.

By providing your email, you are consenting to receive communications from Wealthsimple Media Inc. Visit our Privacy Policy for more info, or contact us at privacy@wealthsimple.com or 80 Spadina Ave., Toronto, ON.

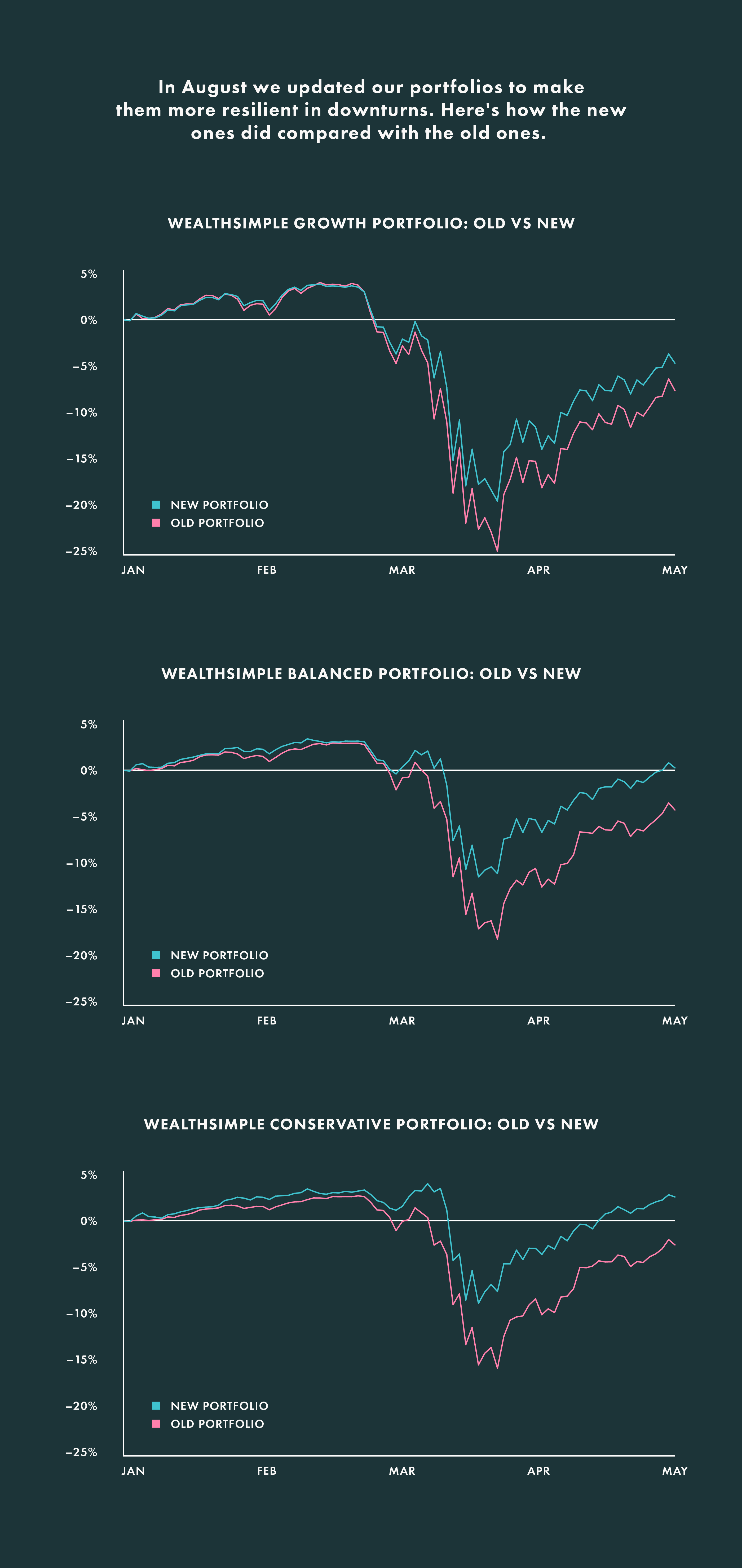

Our Old Portfolios vs. Our New Portfolios

We’re happy to report our portfolios did what we designed them to do. First, some top line numbers. The TSX has declined -12.3% year-to-date (as of April 30). Both our old and new portfolios would have cushioned that blow, but our new portfolio did a far superior job. Year-to-date (again, Jan 1-Apr 30) our old conservative portfolio would have lost -2.6%; our new conservative portfolio, on the other hand, earned a +2.6% return. Our old balanced portfolio would have lost -4.3%; our new balanced portfolio earned +0.3%. Our old growth portfolio would have lost -7.6%, our new growth portfolio declined a more modest -4.6%. (Those returns, by the way, include all the fees you’d pay.)

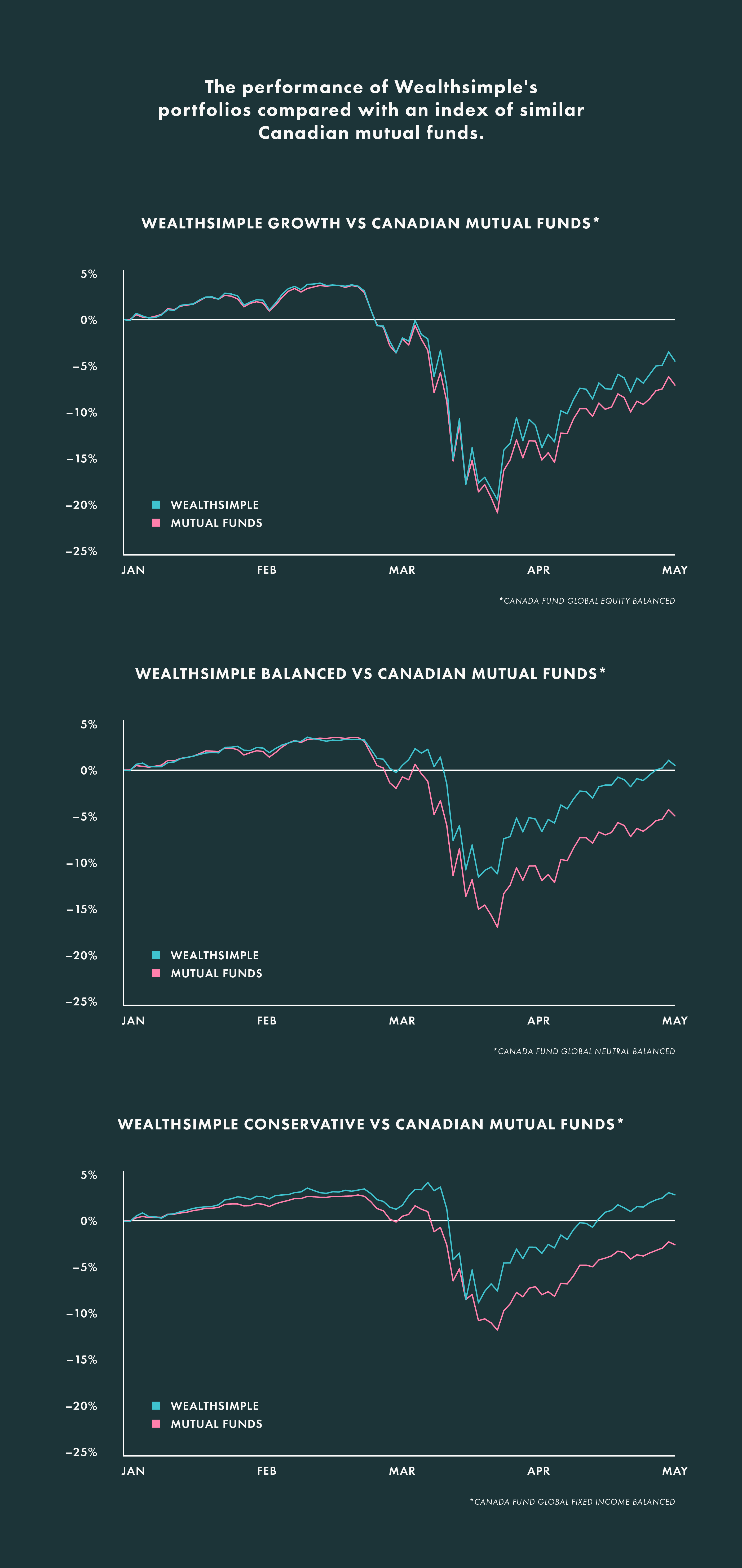

Our New Portfolios vs. Mutual Funds

We also think it’s worth comparing our new portfolios against the most popular way for Canadians to invest money: mutual funds. The easiest way to do that is to chart Wealthsimple’s performance against something called the Canada Fund Global indices — which is a composite of the performance of all of Canada’s mutual funds (specifically the ones that invest in a mix of stocks and bonds) so it’s easy to see how mutual funds have performed. We think it’s a good comparison since one of our core principles is that humans are not that good at picking stocks (the investments in most mutual funds are hand-picked by fund managers), and it’s not worth paying higher fees for them to do it. Here’s what that looks like:

To keep you from having to squint too hard at those graphs, here's how the numbers net out: year-to-date, growth mutual funds lost 7.0% compared to a loss of 4.4% for Wealthsimple’s growth portfolio; balanced mutual funds lost 4.9% compared to a 0.5% gain for Wealthsimple’s balanced portfolio; conservative mutual funds lost 2.5% compared to a 2.8% gain for Wealthsimple’s conservative portfolio.

There’s an important asterisk here. Those returns are what you’d see before you pay fees. If you include the cost of fees, the difference would be even more striking. Wealthsimple’s fees vary slightly by portfolio type, but are a grand total of about 0.65% of your holdings annually. Mutual funds, on the other hand, charge a median fee of 1.94%, about three times as much. And most investors pay an advice fee on top of that.

The Lesson: How investments perform in downturns may be more important than how they perform in rallies

Now look. As we just saw, everything can change in a heartbeat. And like disclaimer lingo has said since time immemorial, “past performance is no indication of future results.” If you’re looking at those graphs and saying to yourself, “Oh good, Wealthsimple will always have better performance than the broader market and mutual funds!” you’re missing the point. We do not think our investments are always going to outperform other investments in a given quarter, or a given year, or even a three year period. But we do think that our portfolios will tend to outperform most conventional portfolios in down markets, and to slightly underperform in up markets. Why do we want to do that?

Here’s the part where we talk about bigger investing lessons: how you do in a downturn is really important. Arguably more important than how you do during a rally. Why? First, if you’re retired or close to being retired — or if you need to spend your money in the near-term — you really don’t want to incur big losses. But it’s also true for folks who are still decades away from retirement. It’s a tricky statistical concept, but every portfolio carries risk of a bad outcome (we show clients this possibility by giving a range of outcomes instead of a simple projected return), and minimizing big losses makes that risk significantly smaller than riding the ups and downs of the market at large. And the last reason is the most human: opening up a statement and seeing huge losses is traumatic, as many of you have probably experienced in the last month or two. Human emotion is the enemy of smart investing, and feeling scared by losses can cause people to do things like pulling their money out of the markets, thereby locking in losses and/or missing rallies. When we all know by now the smartest thing to do is make a long-term plan and stick to it.

We’ll leave you with the promise that we’ll continue to examine and improve our portfolios. (For instance, as mid- and long-term government bond yields approach zero, which is highly unusual, we realize they may not provide the intended diversification.) And that we’ll keep you apprised of whether our portfolios are doing their jobs being as pleasantly boring as possible.

A note about how to understand the graphs above comparing Wealthsimple portfolios and Morningstar's indices of mutual funds. The numbers show performance gross of all fees - meaning before fees are taken out. Wealthsimple's Growth portfolio (80% equity) is compared with Morningstar's index of Canadian Global Equity Balanced funds, which contains global asset allocation funds with more than 60% and less than 90% of their assets in equities. Wealthsimple's Balanced portfolio (50% equity) is compared with Morningstar's index of Global Neutral Balanced funds, which contains global asset allocation funds with more than 40% and less than 60% of their assets in equities. Wealthsimple's Conservative portfolio (35% equity) is compared with Morningstar’s index of Global Balanced Fixed Income funds, which contains global asset allocation funds with greater than 5% and less than 40% of their assets in equities.

Throughout, the indicated returns are historical total returns for the period indicated including changes in unit value and reinvestment of distributions.

Written By

The Editors

Wealthsimple's education team is made up of writers and financial experts dedicated to making the world of finance easy to understand and not-at-all boring to read.