News

Announcing the Wealthsimple Foundation

We want to help one million children from low-income families save for their education over the next 10 years. It's going to be a long journey, but we think it's an important one.

Wealthsimple makes powerful financial tools to help you grow and manage your money. Learn more

It's an article of faith that education is one of the most powerful methods we have to make the world more equal, more just, and more fair. And for good reason — it's true. If a society can't provide an equal opportunity to learn, it tends to become a place you don't want to live. But you know what gets a lot less play? Maybe because at first blush it sounds a little wonky? The very specific, very practical power of an educational savings account to change the trajectory of a human life — and a nation.

An education savings account is more than just money. It's more than just being smart about the future and taking advantage of tax breaks and being a good financial planner. When a kid has money in one of those accounts, it makes it far more likely that she or he will go on to get a degree of one kind or another. That's true even when you control for all other factors — income, parents' education levels, etc. An account like this changes how we think about ourselves, our kids, our futures. And at Wealthsimple we believe that if we can help more people take advantage of that power — and help them fund those accounts — we could help make a profound change in our society. That's why we decided to begin building the Wealthsimple Foundation.

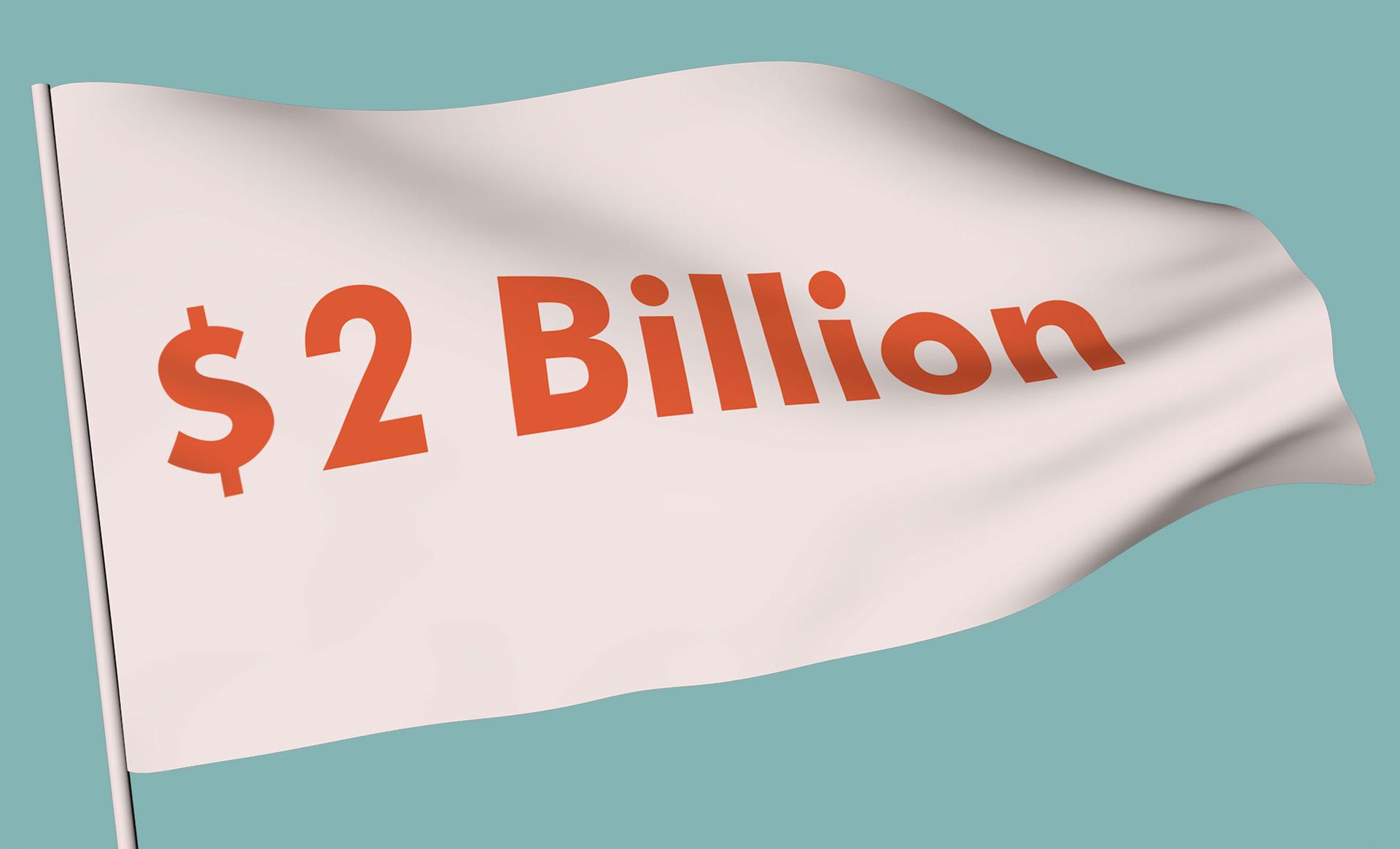

In 2018, $4 billion of CLB grants remained unclaimed because an estimated 1.8 million children who were eligible for the CLB benefit didn't sign up for it.

Sign up for our weekly non-boring newsletter about money, markets, and more.

By providing your email, you are consenting to receive communications from Wealthsimple Media Inc. Visit our Privacy Policy for more info, or contact us at privacy@wealthsimple.com or 80 Spadina Ave., Toronto, ON.

So how does it work? Well, in some respects, we're already lucky. The Canadian government offers all its citizens the RESP, one of the world's most innovative social programs for education savings. The RESP is an account you can use to save money for your child's education. When you take advantage of it, not only is the investment income you earn tax-free, but the Canadian government will also contribute money — a total of as much as $7,200 per child in matching funds to be used toward education. Canada realized, though, that one of the problems with the account was that you could only use it if you had money to save for your children; so it tended to concentrate benefits among families that arguably needed it least. To address that problem they introduced the Canada Learning Bond (CLB) in 2004. The grant promised to deposit $2,000 into the RESP of any qualifying children from low-income families to help level the education savings playing field. Assuming a fairly conservative 5% annual investment growth, an 18 year old who’d received this grant at birth would collect almost $5,000 in grant money towards her higher education, enough to get pretty close to covering a full year of average undergraduate university tuition — $6,838 for the 2018/2019 year. And it's about more than the government's money: CLBs change savings behaviour. 76% of families that get the grant also make their own contributions — the average is $1,100 per year.

But there's a problem. Not as many people use education savings accounts — or get the grants that come with them — as they should. And the ones who do are still largely those with more resources. Wealthier families are 50% more likely to open RESPs for their children. Wealthier kids receive 71% of the available grants from the government. And consider this: in 2018, $4 billion of CLB grants remained unclaimed because an estimated 1.8 million children who were eligible for the CLB benefit didn't sign up for it. In fact, only 35% of children who qualified for the grant claimed it. That's because lots of folks simply weren't aware, or were intimidated by the process of applying for the grants. That shortfall not only helps lock kids into cycles of poverty, it also creates a society of unequal opportunity, and one with greater income inequality. That's a toxic combination.

Here at Wealthsimple one of our founding principles is the importance of an equal playing field. We started this company to make sure that everyone had access to the powerful wealth-building tools that typically only the rich get to take advantage of. That's why our fees are low and we have no account minimums. We’re aiming to bring that same spirit of innovation to tackling the national education crisis.

Today we’re officially launching the Wealthsimple Foundation with a simple goal: we want to help one million children from low-income families save for post-secondary school over the next 10 years.

It’s a big undertaking, but nothing worthwhile is easy. We've started by making the process easier. Traditionally, families had to visit a bank branch and fill out a bunch of paperwork to open an RESP and apply for grants; but we let families sign up at home, in about ten minutes. And the foundation we've started will let us put the innovative thinking we've used to tackle one problem — that a lot of people lack access to good investing tools — to tackle the problem with education funding. We're testing innovative approaches to encourage RESP enrollment with forward-thinking partners, and we're starting with a pilot partnership with Pathways to Education, an organization focused on breaking the cycle of poverty through education.

We're going to have a lot more news soon, so watch this space for more specifics about how you can get involved. Sign up here to find out what we're up to.

Written By

The Editors

Wealthsimple's education team is made up of writers and financial experts dedicated to making the world of finance easy to understand and not-at-all boring to read.