Money & the World

Most of Our Clients are Men. We Wanted to Figure Out the Problem.

We took a hard look at our clients, and people like them throughout Canada, to investigate the problem of women, investing, and the great Canadian wealth gap.

Wealthsimple makes powerful financial tools to help you grow and manage your money. Learn more

Wealthsimple has a pretty simple mission: to give everyone — no matter who you are or where you come from — the tools to gain true financial freedom (while also becoming a successful and beloved company along the way, of course). It’s right there in our culture manual.

Part of our job is to ask ourselves: Are we fulfilling our mission? One way to answer that is to look at the data. We have a hundred thousand clients now — and that means a lot of data about who uses Wealthsimple, and how. And when we look at that data, we see something kind of troubling: Men make up a substantially larger proportion of our clients than women.

That seems like a failure to us. And we wanted to know more about what it means.

Sign up for our weekly non-boring newsletter about money, markets, and more.

By providing your email, you are consenting to receive communications from Wealthsimple Media Inc. Visit our Privacy Policy for more info, or contact us at privacy@wealthsimple.com or 80 Spadina Ave., Toronto, ON.

So we hired Leger, one of Canada’s premier research firms, to help us get some deeper insights into gender and money and the way those things relate to each other. We now have those results, and there are some surprises.

Part One: The Problem

The first part is pretty simple. We have substantially more male clients than we do female. How substantial? There are almost twice as many men.

67% of our clients are men. 33% are women.

Part Two: Is It Just Us?

We think that’s a problem — from a social perspective and from a business perspective. But we were curious: Was this a Wealthsimple phenomenon? Or was it something bigger? So the first thing we had Leger do was to figure out how our numbers compared with the world at large. So we started polling.

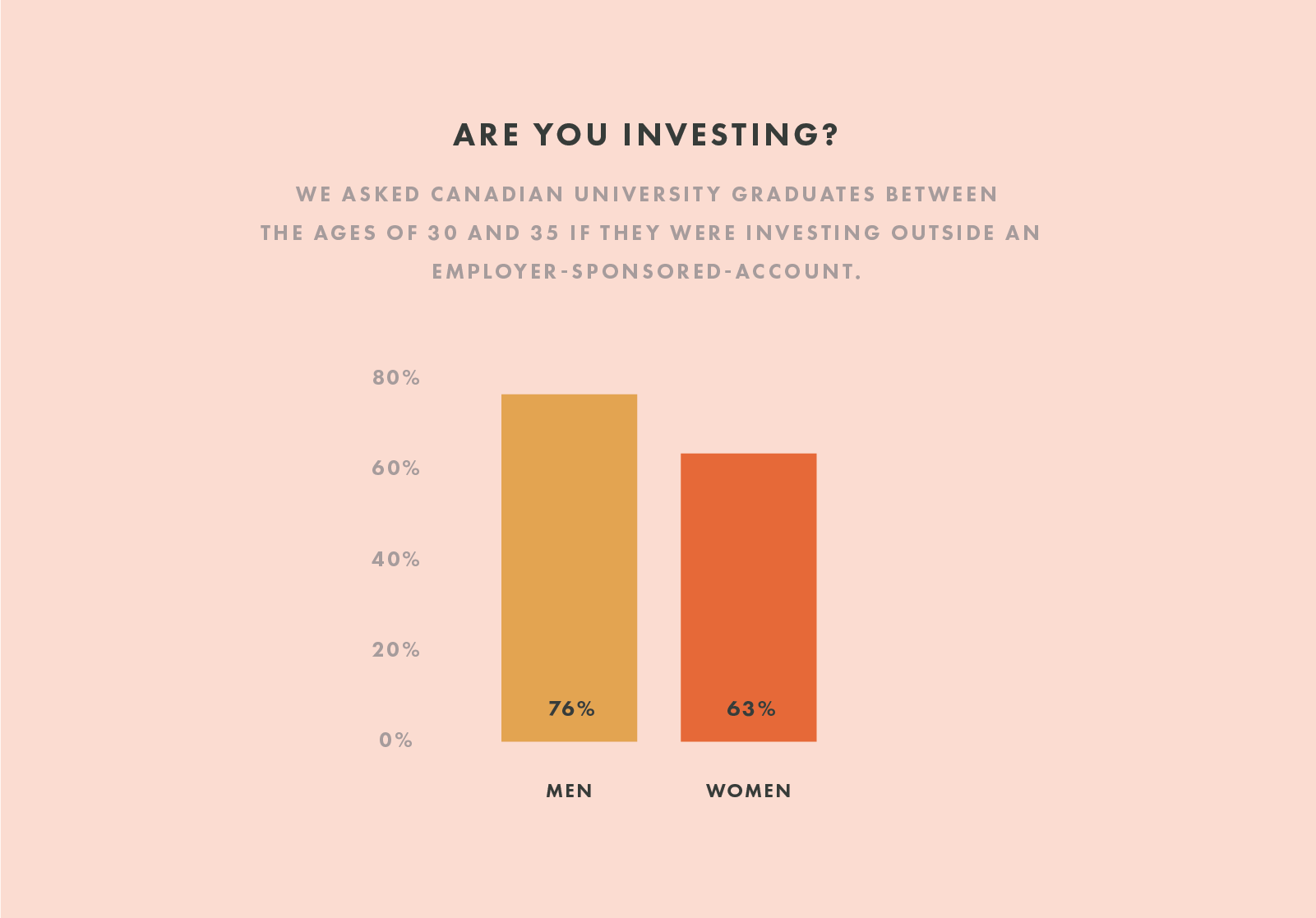

First we selected for Canadians that were an awful lot like the typical Wealthsimple client: people between the ages of 30 and 35 with a university degree. Why did we conduct the research ourselves? Because we wanted to do some pretty specific work: We needed to strip away as many other variables as possible so we could focus on these gender differences. We wanted to pick a group of people to poll who were all on relatively equal footing — folks who graduated from a four-year degree program in Canada about a decade ago. Inthe years since, as they paid off their loans, got first jobs, got better jobs, we wanted to know how they diverged.

What did we discover?

The good news is that it’s not just us. The bad news is also that it’s not just us. Take a look at the graph below:

Part Three: So How Bad Is It?

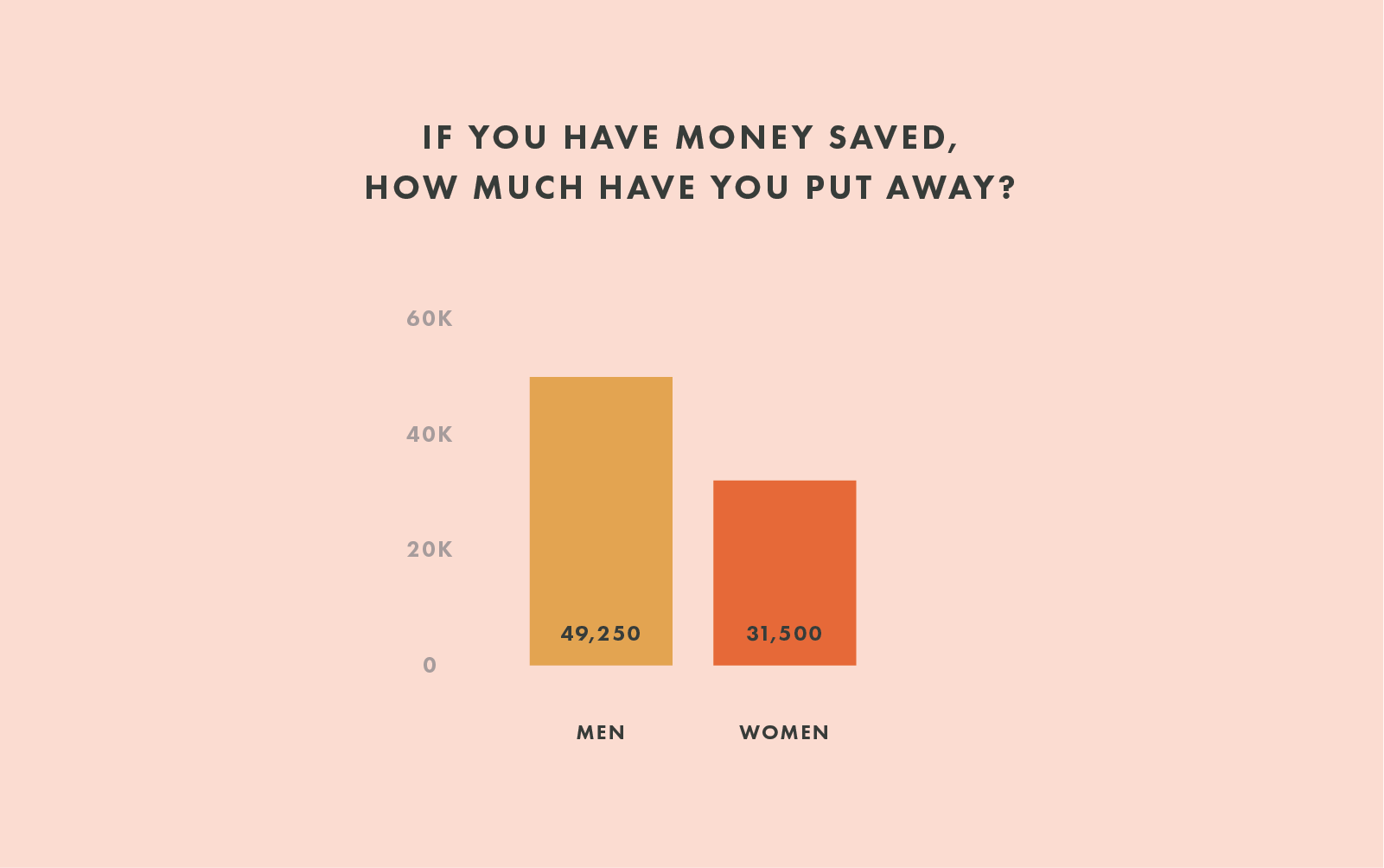

We dug a little deeper. Saving money, and investing money, isn’t only binary. Whether we do it or don’t do it is important, but how much we save and invest is also very important. So we asked that.

Among the men and women who said they saved money, men had saved more. The men we polled had saved an average of more than $49,000. The women had saved a bit more than $31,000.

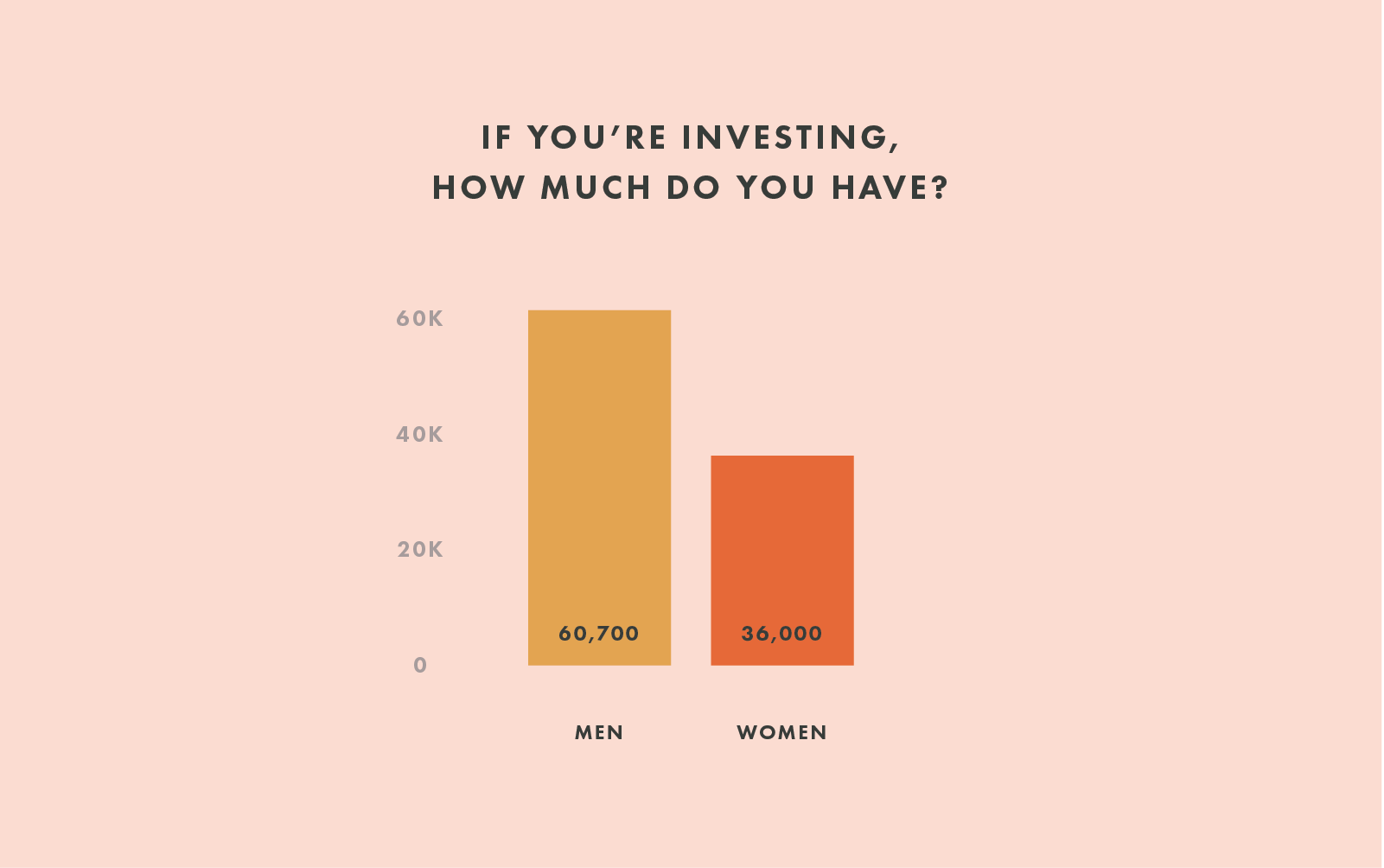

And again, not all savings are created equal. Over time, money that’s invested in markets tends to grow at a significantly higher rate than money that’s been sitting in a savings or chequing account. So we asked all the people who told us they were investing: Just how much do you have in your investment accounts? Again, men far outpaced women — an average of more than $60,000 for men; an average of $36,000 for women.

Part Four: How the Savings Gap Becomes the Wealth Gap

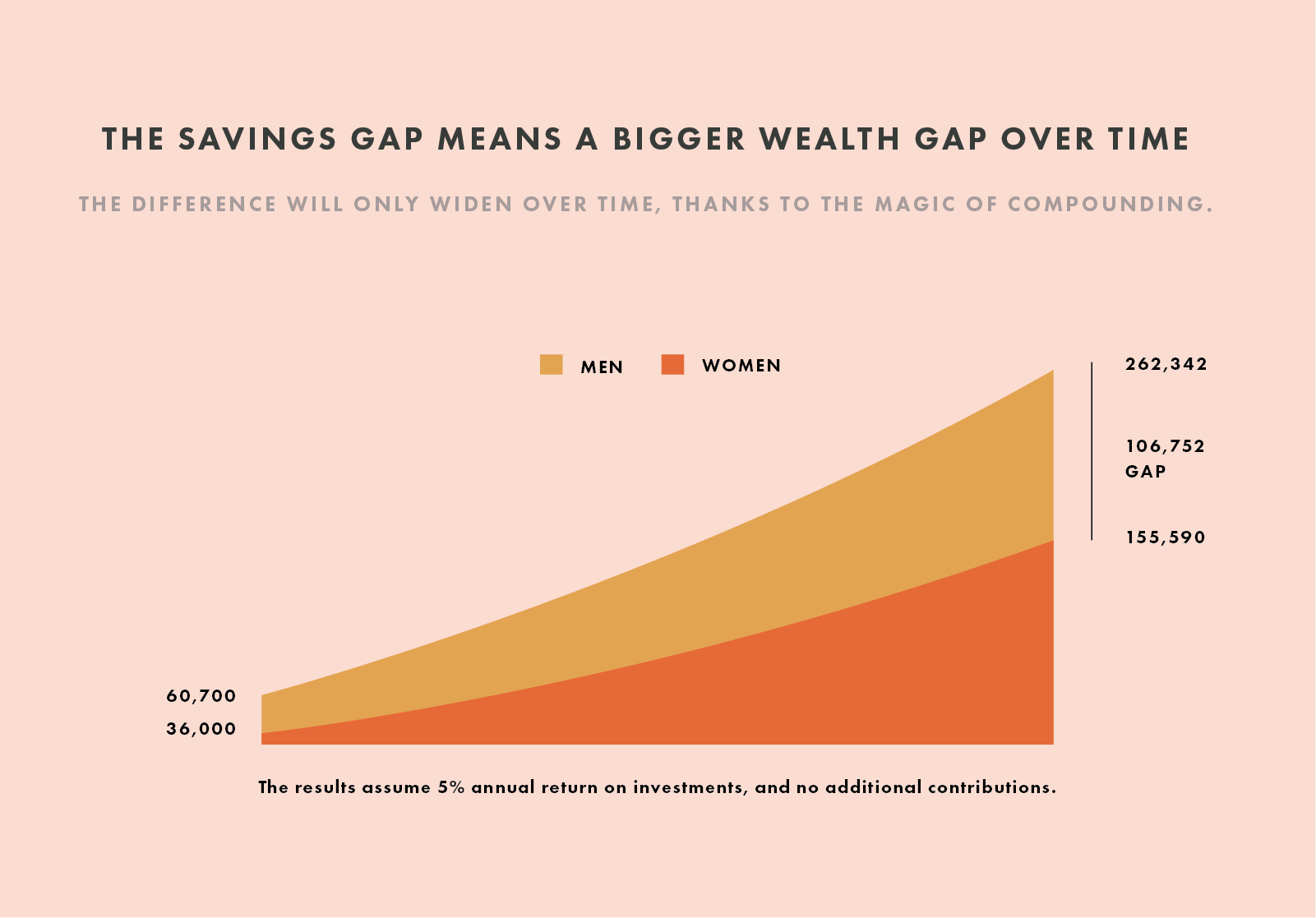

One of the first bits of advice we give to any prospective client is: Start saving and investing as soon as you can. Even if it’s not much, that little bit gets bigger over time, thanks to the magic of compounding. That means that women are missing out on an opportunity to build significant wealth, creating a significant gender wealth gap.

Let’s break it down. As we showed above, the average 30- to 35-year-old man who is investing has put $67,000 into his investment accounts. The average woman investor has put only $36,500. That’s a difference of $30,500. But, even assuming they both stop there (instead of continuing the trend of men investing more each year than their female counterparts), that difference balloons to $106,752 over 30 years. That’s like five new cars, a decent down payment, or, you know, just a pretty nicely elevated quality of life.

Part Five: So Why Is This Happening.

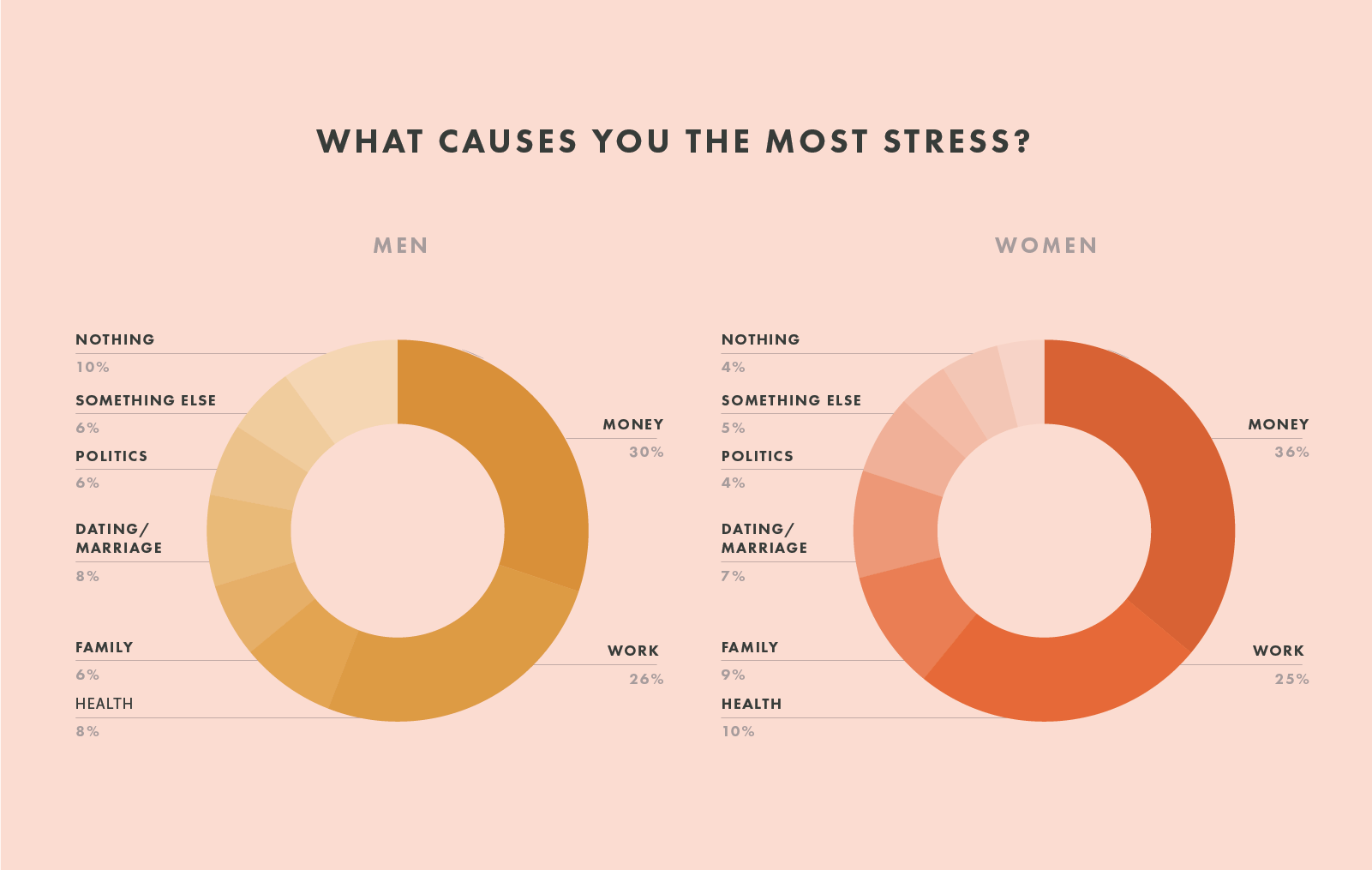

We wondered: Were women just less worried about money than men? Maybe they’re not saving as much because they’re much less materialistic, anxious, or otherwise fixated.

Well, the numbers don’t support that. More women than men polled said that money was their biggest stressor. Again: It’s not simply something they worry about, but the thing they’re most worried about.

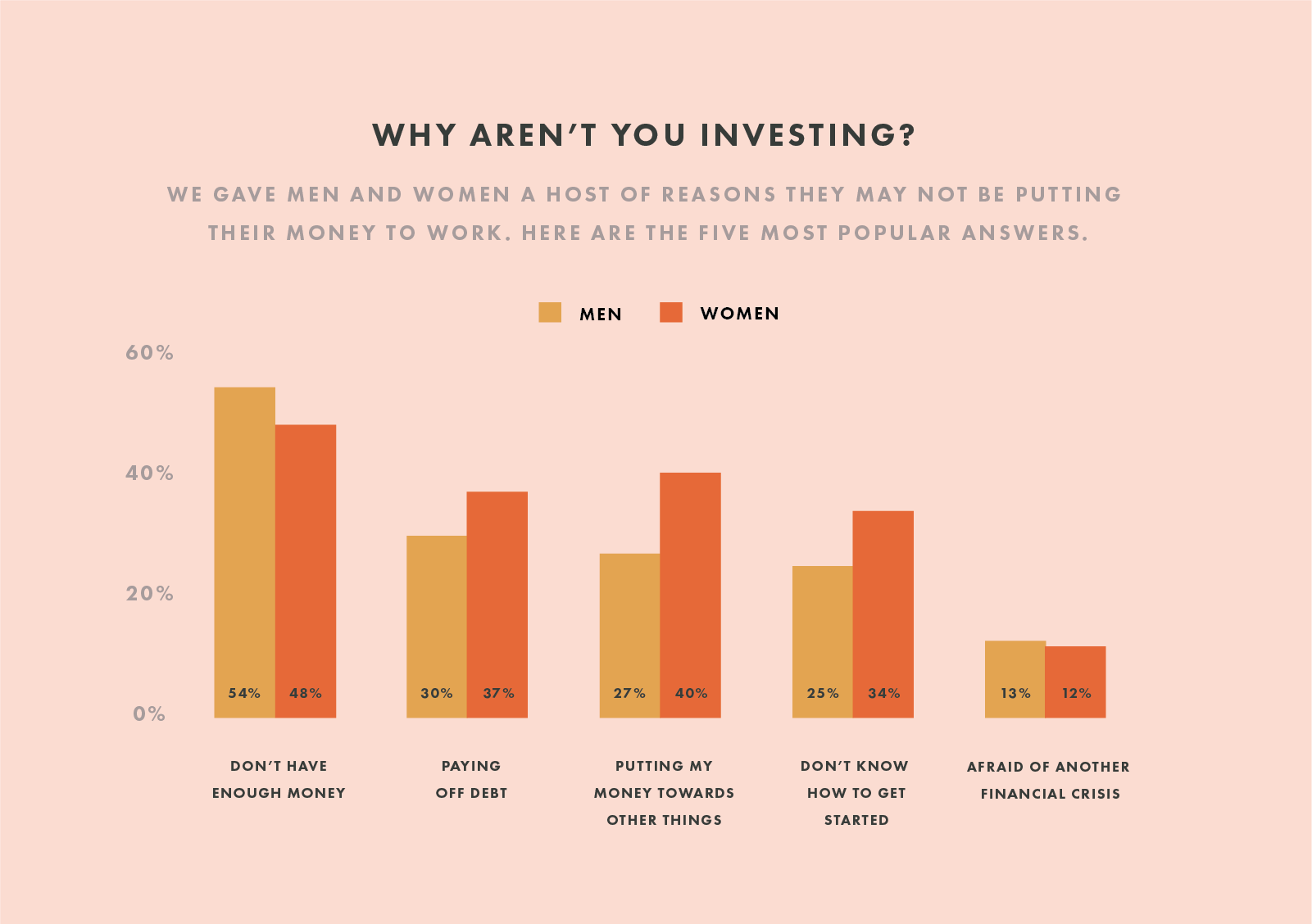

To find out more, we asked about what keeps people from investing. Here’s what they said.

One of the numbers that stuck out to us was the number of respondents who said they weren’t investing because they don’t know how to get started. About 50% more women than men said this was the case. We think that might be related to some other findings from our poll: Women are less likely to talk to their friends about money than men are; men are more likely than women to use personal finance books, blogs, media, and their friends for money advice.

Part Six: Is There Any Good News Here?

The first bit of good news is that women have more money now than ever before. In fact, by 2024, Canadian women will hold half of the country’s private wealth. Second, women are investing, and they’re investing young — the average age they start is 25.

This isn’t related to the wealth gap, but as long as we’re talking about changing the world: Our client data shows that women are significantly more likely to choose socially responsible investments.

We think the first step toward change is what you’re doing right now. Educating yourself. Starting the conversation. We're working with partners to help us do that with a wider audience. We are changing the makeup of our team at Wealthsimple — if we want products that appeal to the world at large, our team needs to better reflect that wider world. And we’re conducting research like the study you’re reading about right now, so we can better understand what’s wrong and how to fix it.

We know you work hard for your money. So we want it to be easier to make your money work for you.

Written By

The Editors

Wealthsimple's education team is made up of writers and financial experts dedicated to making the world of finance easy to understand and not-at-all boring to read.