Money Diaries

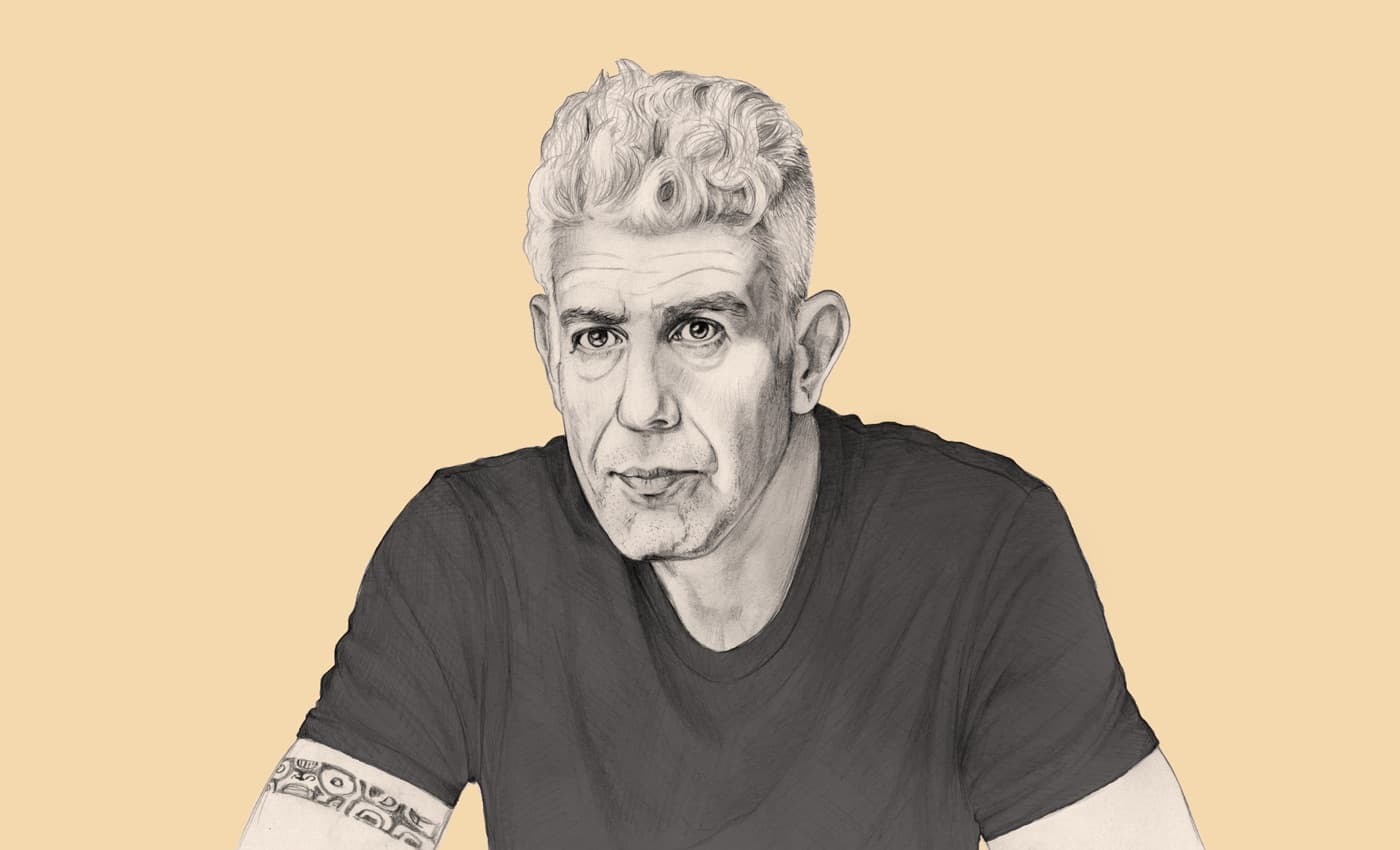

Anthony Bourdain Does Not Want to Owe Anybody Even a Single Dollar

Before he was the guy from Parts Unknown, he was 44, never had a savings account, hadn't filed taxes in 10 years, and was AWOL on his AmEx bill. That turned out to be a great financial education.

Wealthsimple makes powerful financial tools to help you grow and manage your money. Learn more

I don't want to sound like I’m bragging about this, but the sad fact is, until 44 years of age, I never had any kind of savings account. I’d always been under the gun. I’d always owed money. I'd always been selfish and completely irresponsible.

I grew up decidedly middle-class. At the time of my birth, my dad worked days in a printing company, and at nights at a Sam Goody record store. My mom was a magazine and newspaper editor. It was a very different America: the middle class of those days seemed somehow more aspirational. They read Cheever and Updike and tried to stay up on culture. We barbecued in the backyard, vacations were at the Jersey Shore in shared two-family homes. Was I aware of money? Yeah. I was aware we didn’t have enough sometimes.

I didn’t put anything aside, ever. Money came in, money went out. I was always a paycheque behind, at least.

My parents were not good with money. My father was a dreamer who didn’t seem to think or talk about financial things. My mother was far more organized, but I think her aspirations outpaced her ability to pay. They bought things they couldn’t afford. They put me in a private school, and I know they had problems paying the tuition. We had a Rover sedan at one point, and the upkeep for an unusual foreign car was a big burden. We inherited some money at one point, and a major renovation of the house happened—extensive landscaping, a full build-out. It took years, followed by a period of financial struggle. In retrospect, maybe we could have done without the shrub pines.

I had a paper route at various times. I was a bicycle messenger in New York during summer and Christmas vacations. I was a shitty messenger because, free in New York without supervision, I’d just buy loose joints for a dollar and go to the grind houses, where it was a triple bill—Bruce Lee, Melvin Van Peebles, and a revival film—all for three bucks. The drinking age was 18 at the time, and somehow, at 14, I could pass. As a bicycle messenger, you only worked as much as you liked. So, I worked a little. I was not exactly the most motivated bicycle messenger in the world.

I was aware that I had far less money at my disposal than just about everyone I went to school with. They lived very different lives, which was a real eye-opener. I was from a more middle class town, Leonia, New Jersey. And the kids who lived there, we had a carpool to take us to Englewood School, the private school where some of us went. Our houses smelled of breakfast, of bacon. The wealthier kids’ houses smelled different. They dressed differently. We were not poor. I don’t want to give that impression. I was fortunate, but envious. When my father drove me to school, it was often in an old station wagon with the side door bashed in, which we didn’t ever seem to have the money to repair. Most of the kids at my school got a sports car as soon as they got their permit. Most came from broken homes, but lived in fabulous houses. They had lives unbothered by loving parents, where they were free to watch pornography and do drugs and misbehave. I envied them that. My friends could afford weed and cocaine. That was certainly a motivator, maybe a bad one, but a not unimportant one: my friends could afford drugs, I could not. They would share but, of course, the thing about cocaine is that you can never have enough.

I am fanatical about not owing anybody any money. I hate it. I don’t want to carry a balance, ever.

Sign up for our weekly non-boring newsletter about money, markets, and more.

By providing your email, you are consenting to receive communications from Wealthsimple Media Inc. Visit our Privacy Policy for more info, or contact us at privacy@wealthsimple.com or 80 Spadina Ave., Toronto, ON.

My father went to Yale for two years, then dropped out. My mother went to Hunter College. I grew up in Kennedy times, when it was repeatedly assured, almost as a birthright, that all children would have better lives than their parents. So it was assumed I would go to college from the very beginning. And somehow, my parents paid for the brief time I was enrolled. I don’t know how they did it — I wasn’t asked to contribute. I think they recognized that I was a lazy, good-for-nothing shit who could not be counted on to raise money for college.

During my second year, I approached my parents in a vulnerable moment. They were struggling to pay tuition, and my brother was about to start college, too. He was going to do well; I clearly was not. I was a waste of money and of an education. So, when I said, “I’m going to drop out,” I’m sure they were relieved. Somehow they found the bucks to pay for cooking school tuition, which was also hard for them.

In cooking school, I’d work weekends in New York as a cook; I think I was paid $40 cash per shift, which was a lot at the time. I made extra money by playing poker and Acey-Deucey, another card game. I may or may not have moved a little product. I graduated and went right to work, five, six days a week, often 12 hours a day. At first, after taxes, I never went home with more than 120 bucks. Not a lot of dough. I was staying with my then-girlfriend. I scrounged. Slowly, over time, I transitioned into a rent payer, such as I could. I ate most of my meals at work, or from the falafel place, the bagel place or the diner. Weed was a major expense. Before I reached the point where weed made me paranoid and agoraphobic, it was costing me a few hundred dollars a week. Looking back, the fact that I'd been smoking weed heavily since I was 14 might have had something to do with my relative lack of ambition. Just saying.

I didn’t put anything aside, ever. Money came in, money went out. I was always a paycheque behind, at least. I usually owed my chef my paycheque: again, cocaine. Like I said, until I was 44, I never even had a savings account.

When I was a working cook and chef, going to the Caribbean was always the great indulgence. I’d find myself either with a fresh credit card, or maybe having somehow paid down the previous one though I don’t remember actually ever doing that. We’d go to the Caribbean, stay as long as possible, and burn through all the credit on a card. I’d have to quit my job to go, but when I came back there was always work. I changed jobs an average of about once a year.

I was constantly in debt. I published a few books before Kitchen Confidential, but they were not financial successes. I was given a $10,000 advance for Bone in the Throat, which I split 50-50 with my old college roommate, who got me into book publishing. For the second book, Gone Bamboo, I probably walked away with around eight grand. When Kitchen Confidential was published, I hadn’t filed taxes in about 10 years. I was seriously behind on rent. It had been about a decade since I’d communicated with American Express in a timely manner. In my daily life, the goal was to muffle the anxiety that I’d feel as I tried to drift off to sleep knowing that, at any point, what little money I had in my bank account could be garnished by the IRS or the credit card company. The landlord could kick me to the curb. That was my reality for many years.

At the end of my cooking career at Les Halles I went home with about $800 and change per week, after taxes. Briefly, near the end, I got on the group health plan. Before that, I never had health insurance, other than at the Rainbow Room, where you went to this horrifying union clinic; there were set amounts paid for different types of injuries. A guy caught his finger in the oven door and yanked the tip off, because there was more money in a partial amputation. So health insurance has been this incredible new thing for me, in my life only since about 2001.

I think living like that made me very cautious. I held onto my job after Kitchen Confidential came out; I was hesitant about whether I should leave the kitchen, and I waited as long as I could. I was old enough to realize I’d been handed this incredible, lucky break and I was very unlikely to get another one. There was this weird moment where I noticed that everyone in the dining room were journalists waiting to talk to me, and I realized I’d become the sort of chef I used to despise, constantly having to leave the kitchen to deal with journalists. I didn’t want to be that guy. So I left. Once I did that risky thing, leaving the only profession I knew to become a professional writer and TV guy, I was, and continue to be, very careful about the decisions I make every day.

A friend said, “You live outside the country more than half of the year. Create a bogus residence in the Caymans and pay no U.S. taxes.” I’d feel like a shit doing that. I’m an American. I don’t want to be that guy.

That was really the first time I started thinking about saving money. About not finding myself in that terrifying space, that uncertainty that goes back to childhood. Will the car get fixed? Will we be able to pay for tuition? In very short order, I contacted the IRS and I paid what I owed. I paid American Express. Since that time, I am fanatical about not owing anybody any money. I hate it. I don’t want to carry a balance, ever. I have a mortgage, but I despise the idea. That was my biggest objection to buying property, though I wasn’t in the position to pay cash.

The reports of my net worth are about ten times overstated. I think the people who calculate these things assume that I live a lot more sensibly than I do. I mean, I don’t live recklessly — I have one car. But I don’t deprive myself simple pleasures. I’m not a haggler. There’s not enough time in the world. I tend to go for the quickest, easiest, what’s comfortable. I want it now. Time’s running out.

One of the wonderful things about my agent, Kim Witherspoon, is she always presents me with two options when approaching a business deal, particularly when it comes to books. She’ll say, ”Look, you could go with these guys and get a whole shitload of money upfront, or you could go with these guys, which is the morally right and loyal thing to do, and negotiate an amount of money that fits in with what we actually think you’re going to sell.” I like to make money for my partners. Publishing is filled with stories of people who do well with a first or second book, then get like some huge advance that they can never earn out, which leaves them, and their publisher, in a bad place. My book imprint — it’s called Anthony Bourdain and it’s at Ecco Press — makes almost no money for me, but it’s deeply satisfying. I do it for love, and for reasons of advocacy. There are people out there whom I feel should champion. And it’s just creatively and personally satisfying to help people get heard. I bask in the collective glory when somebody puts out a good book on my imprint. But there’s no money in it.

Writing a book is probably the least bang for the buck. My Get Jiro co-author Joel Rose talks about this: you spend a year of your life, or more, writing a book. You get a chunk of money and they put it out there, and the overwhelming likelihood is you’re going to get very little back. My books do very well, but it’s probably the least profitable thing that I do. I like writing. But writing your way to riches isn’t a reasonable life plan. For me it's responsible for everything though. I started out doing book tours; they became too big for the bookstores, so they would rent halls, which would fill. Those numbers grew and grew, and people started booking me for corporate events, which were incredibly lucrative. And then people who promote concerts and musical acts approached me. It quickly became clear that, like the record business, there ain’t no money in a record. It’s the tour. The biggest revenue stream out there for me is going out and telling dick jokes. It’s physically and mentally punishing, and takes a lot out of me, but it's over in a relatively short period of time.

I’d like my daughter and her mom looked after, both while I’m alive and after. They shouldn’t have to worry if something bad happens, so my investments and savings are based on that. I’m super-conservative. Money doesn’t particularly excite or thrill me; the making of money gives me no particular satisfaction. To me, money is freedom from insecurity, freedom to move, time if you choose to make use of time. My investments advisor understands that I’m not looking to score big on the stock market or bonds. I have zero understanding of it and zero interest. Life is too short. I like a limited amount of mail, and a limited amount of conversations with people who make the investments. If the money’s not less money every time I look at it, I’m pretty happy. If it’s a little bit more, great.

I kid that I like to be a patriarch. I like the idea of retiring on a hilltop, surrounded by people I care about, but the fact is, I like working with the people I work with because they’re talented people who could easily make just as much money working elsewhere, if not more. The people who work with me on my TV show in particular: these motherfuckers could get paid a lot more money making a less good show for somebody else. So the pressure’s on me to be the sort of person people will want to stick with.

Nobody likes paying high taxes, but I don’t mind. Maybe that’s a luxury, but I don’t need to hire some hotshot to spend 12 hours a day figuring out how to chisel the government out of an extra few thousand dollars. If getting that extra money means a lot of phone calls and talking to financial analysts and lawyers, I don’t want it.I don’t want to have those conversations. A friend said, “You live outside the country more than half of the year. Create a bogus residence in the Caymans and pay no U.S. taxes.” I’d feel like a shit doing that. I’m an American. I don’t want to be that guy. I don’t want to have those kinds of conversations. I’m putting myself to sleep just thinking about it. I’d rather make a lot less money. It’s honest dollars. Everybody gets theirs: my partners make money, I make money, the government gets theirs. If they call me in for a full audit, great, here I am. It’s all there. I lived a lot of years afraid of the bank, the landlord and the government calling. Nowadays, it’s nice to not be afraid.

As told to Laurie Woolever exclusively for Wealthsimple. Originally published March 14, 2017.

Written By

Laurie Woolever

Laurie Woolever is the author of "Care And Feeding" and "Bourdain: The Definitive Oral Biography." She served as Anthony Bourdain's assistant and co-author for nearly a decade.