Finance for Humans

Why Would I Ever Put Money In Savings Instead of Investing It?

Because a savings account is crucial to any smart financial plan. (That's the reason we launched Wealthsimple Save.) Unless you don't care about risk or making your money make money.

Wealthsimple makes powerful financial tools to help you grow and manage your money. Learn more

I'm going to lead with my major reservation here. The idea of a savings accounts seems a little antiquated to me. I’ve got a chequing account. I’ve got investments. Why do I even need a savings account?

Let's start with an example. Do you know about the idea of an emergency fund?

Let's pretend I don't.

When I do a portfolio review with a client, one of the first things I recommend is to keep enough cash (or cash equivalent) to keep you going between three and six months, in case some emergency happens. Like if you or your spouse lose your job. If that happened and you, for instance, were forced to live on credit cards, the interest might be so crippling it'd be hard for a lot of people to recover.

The perfect place for an emergency fund is savings.

Sign up for our weekly non-boring newsletter about money, markets, and more.

By providing your email, you are consenting to receive communications from Wealthsimple Media Inc. Visit our Privacy Policy for more info, or contact us at privacy@wealthsimple.com or 80 Spadina Ave., Toronto, ON.

But why? Shouldn't I just put that money into — hmm, where did I hear this phrase before — a low-fee diversified portfolio, like the world's smartest investors?

Investment accounts are for longer-term investments. There's risk involved in them, and one thing that decreases risk is time. An emergency fund should be there if you need it.

It’s a good rule of thumb that if you’re going to need money within three years, keep it in either cash or cash equivalent. Some people think a chequing account is a smart place to park that cash. But you earn no interest. That's where a good savings account — where you’ll actually be earning a little bit on your money — comes in. Of course, I'm partial to our product, Wealthsimple Save, because you'll be earning a pretty high rate.

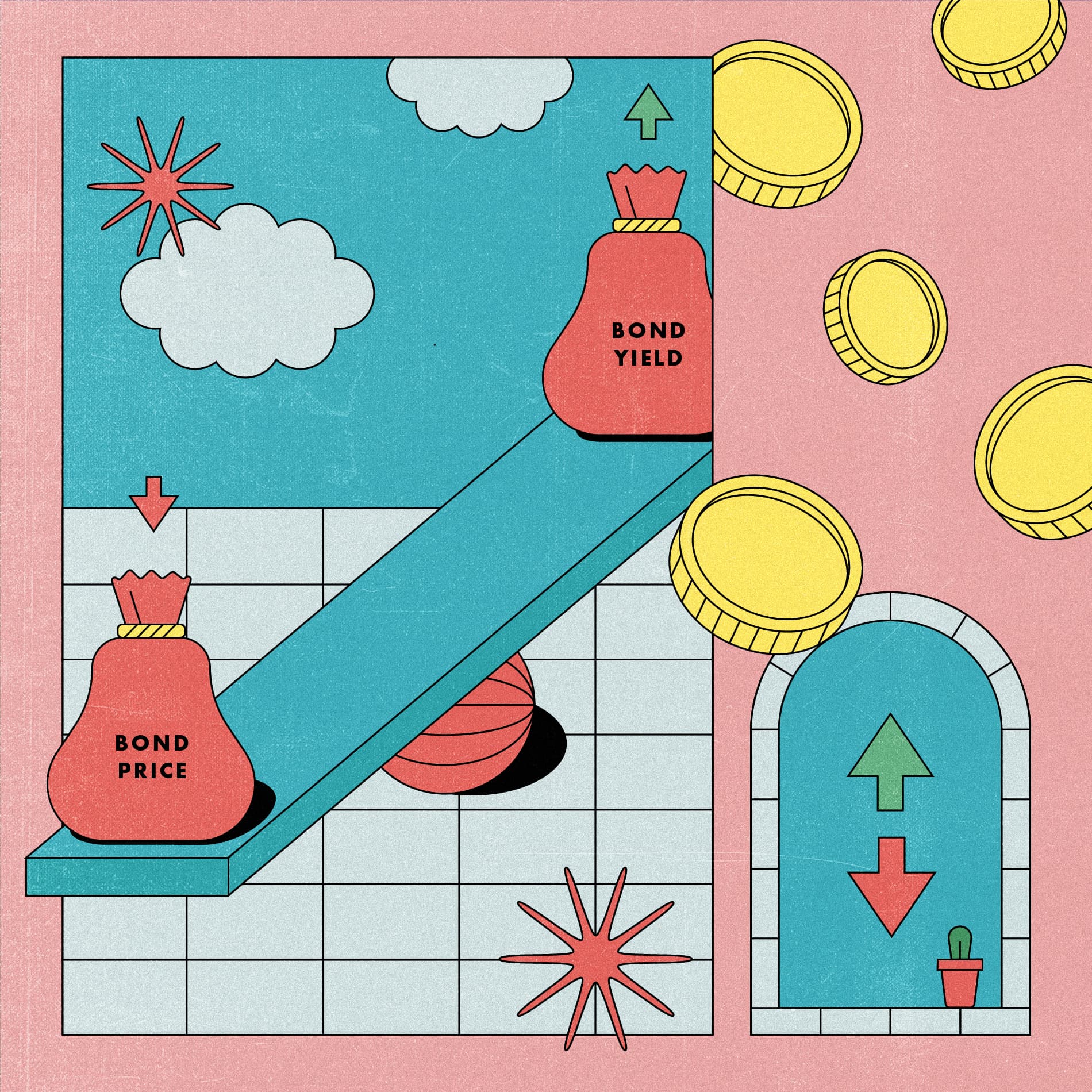

But one of the things you've taught me over the course of our conversations is that, to offset the volatility of owning stocks, it's wise to have some of your investments in bonds. It's part of how Wealthsimple diversifies its portfolios. So why not just put any cash I’ll need in bonds instead, since they are safer than stocks and their rates are typically higher than savings?

Look, you could do that. But the thing you need to understand about bonds they are relatively stable, but you will see fluctuations in prices. Bonds usually go up in value when interest rates go down and down in value when interest rates go up. Take the moment we're living in now: as you’ve might have heard, we’re entering into a financial environment where interest rates are expected to go higher, which means bond prices will most likely will fall. So you may actually experience a loss on the principal of the bond.

The point is: there is some money you want to keep safely at hand while earning as much interest as possible and not have to worry about market fluctuations. That's what savings is for.

Recommended for you

OMG You’re Having a Baby! (A Guide to That and Other Big Life Moments That’ll Affect Your Taxes)

Finance for Humans

The Bond Market Fell, Hard. An Explainer for Normal Humans

Finance for Humans

The Budget for People Who Hate Budgeting (and Also Want a Bidet)

Finance for Humans

The Perfect Guide to Every Little Tax Question You Have

Finance for Humans

OK. So when I have my emergency fund in savings, am I done? Do I ever have to put more money into savings again?

Savings is a smart place to stash any money that you're going to need in the short-term. Money for a down payment on a house you want to buy, money you're planning to use for a vacation. A lot of freelancers I know need to make quarterly payments on their taxes — savings is perfect for that.

I'm a freelancer but I’ve always used a kind of faith-based approach on paying my taxes. I pray to God I have enough money in my chequing account to pay my taxes when they’re due. Why not keep the money in chequing?

Saving the money in your chequing account is dangerous because you're using that account all the time. On the other hand, hopefully you don't take money out of your savings account day to day to pay bills. So you're less likely to spend your tax money on, say, groceries and find yourself behind the eight ball come tax day.

So if we’re entering into a period of higher interest rates, will I be seeing the interest rate on the savings account rise?

Interest rates on savings accounts don’t move in lockstep with rising interest rates set by the Bank of Canada. But in general, you should see your interest rates go up as interest rates in general go up.

I’m Googling as we speak. There are some places that seem to offer really high-interest rates for savings.

I’d read the small print on any ads you see online. A lot of those advertised rates are introductory or “teaser” rates. They're designed to bring you in and then three months later, or six months, or whatever it is, the rates will go down to almost nothing.

A lot of these banks also require minimum deposits of $5 or even $10,000. And then you'll have your money in all these different places and will need to move it around constantly to find the next teaser rate.

No offense, but I think I've figured out the devious plan you guys have concocted. I know your fees are a flat 0.5%. So if I pay a 0.5 % fee, and you're giving me, say, 1% percent a year, then I'm really only making 0.5% interest.

We don't charge 0.5% on savings. The rate we show you already accounts for the fee we earn — 0.25%. With Wealthsimple Save, your rate is your rate.

When I had my money in a good old-fashioned bank account I always liked that it came with protection in case the bank went out of business. Does that go out with window with you guys?

There absolutely is protection. Our brokerage is a member of the Canadian Investor Protection Fund, which covers accounts up to $1M against bankruptcy.

Do I get one of those passbooks? Those also remind me of my childhood. Can you guys whip up one of those for me?

We won’t have a passbook. Sorry. But how’s this: you'll be able to see all your activity — your deposits, withdrawals and your monthly interest — right in the app. It’s even better than a book.

Written By

The Editors

Wealthsimple's education team is made up of writers and financial experts dedicated to making the world of finance easy to understand and not-at-all boring to read.