Finance for Humans

The Bond Market Fell, Hard. An Explainer for Normal Humans

A steep selloff in government securities has unnerved Wall Street — and made individual investors question whether bonds are even worth holding anymore. Here’s what’s going on.

Wealthsimple makes powerful financial tools to help you grow and manage your money. Learn more

Note: This story first ran in TLDR, Wealthsimple’s weekly non-boring newsletter.

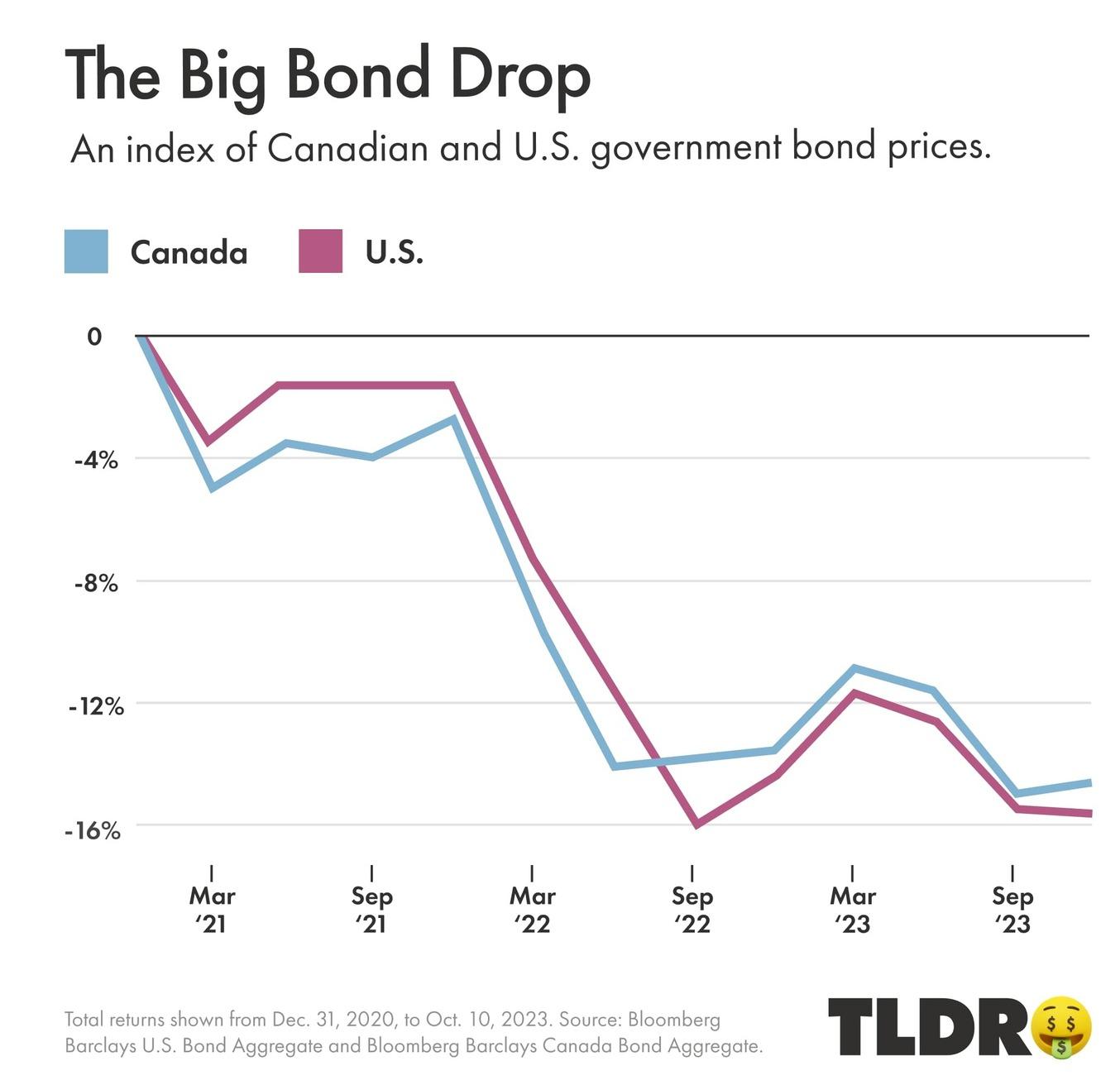

The bond market has been performing worse in recent weeks than pretty much anyone thought imaginable. Take your pick of headlines: it’s a meltdown that rivals the bursting of the dot-com bubble. Or it’s the worst bond collapse in 150 years. Or maybe it’s the worst U.S. bond selloff since 1787. (You did not want to be in fixed income in the late 1780s.) Canadian and U.S. government bonds of all flavours have slid by about 15% over the last three years. Here’s the percentage decline since Dec. 31, 2020:

Now, you might have a question. What is the bond market, and why should I care that it’s making those lines go down? Let’s get into it.

Recommended for you

You Probably Shouldn't Panic Sell to Avoid Drawdowns

Finance for Humans

10 Books That’ll Teach You Everything (Or at Least a Lot) About Money

Finance for Humans

The Budget for People Who Hate Budgeting (and Also Want a Bidet)

Finance for Humans

Make Your Financial Life Bulletproof, With Help From John Goodman (?!)

Finance for Humans

First, what are bonds again? Bonds are essentially IOUs. When you buy a bond, you’re giving governments or companies or whoever the issuer is a loan in exchange for regular interest payments, aka coupon payments. Then, at the end of a predetermined amount of time (when the bond “matures”), the bond issuer gives you back all the money you initially lent out. Before a bond matures, you can also sell it to whoever will take it for whatever amount they’ll pay. When people talk about a bond’s price, they’re talking about what you could sell one of these already-issued, not-mature bonds for. And those prices are what’s falling right now.

Why does that matter? Because if you have your money in a managed fund, or are managing your own money in accordance with the conventional wisdom about portfolio diversification, you probably own bonds because they’re supposed to be stable. Bonds and their reliable lil’ interest payments generally don’t return eye-popping amounts — over the past 70-odd years, bonds on the whole have made about half as much as stocks. But bonds’ interest payments are fixed, and bond prices are typically much less volatile than stock prices. So they’re purchased as hedges against stock downturns.

So why are bonds not boring now? Demand for boring, safe-ish long-term bonds has been strong for the past few decades — so strong that bond issuers haven’t had to offer big interest payments, or yields; at times, yields have been south of 1%. But over the past few years, inflation and interest rates have gone way up, and because of rising rates, investors can now earn a much better return by sticking their cash in a zero-risk savings account or short-term GIC. This is bad for bond prices.

Why? Let’s say you own a $1,000 bond that was issued a couple of years ago. You’ll get paid back the bond’s face value, of $1,000, in eight years, and until then, you’ll earn an annual yield of 1%, or $10. But at this moment, anyone with money in their pocket can earn almost 6%, or $60, on a $1,000 GIC, and they have to lock their money up for only one year. So who’s going to pay $1,000 for your crummy old 1% bond? No one, that’s who! So the price of your bond on the open market goes way down. (Sorry, bond.)

Why are people worried? Falling bond prices can pose a problem for small- and midsize banks, which tend to hold a lot of bonds, believing they’re pretty safe. But when prices fall, they can become insolvent — Silicon Valley Bank lost something like US$21 billion from falling bond values. Meanwhile, anyone issuing a new long-term bond now has to offer a high rate of interest on it, which makes it harder for businesses and governments to borrow money, which slows down the economy. Also, there’s the basic problem that if you’re trying to sell parts of your portfolio for retirement or to make a major purchase, the bond portion of your holdings is worth less right now.

Should I dump all my bonds and/or never buy a new bond again? We don’t give investment advice, but if there’s a recession anytime soon, the stock market would likely lose value and bond prices would probably recover, since investors have historically fled to bonds for safety when stocks fall. If there’s not a recession and you’ve got time to wait, you can just hang onto your bond until it reaches maturity and still get paid back its full original value, so you’re not out anything, really. As for buying bonds, 10-year government bonds are now offering 4% yields, which is lower than cash rates but you can lock in that yield for a decade and who knows what will happen to cash rates over that time. So there’s that to consider.

Written By

Ben Mathis-Lilley

Ben Mathis-Lilley is a senior writer for Slate.com and the author ofThe Hot Seat: A Year of Outrage, Pride, and Occasional Games of College Football. He's also written for BuzzFeed and New York magazine.

The content on this site is produced by Wealthsimple Media Inc. and is for informational purposes only. The content is not intended to be investment advice or any other kind of professional advice. Before taking any action based on this content you should consult a professional. We do not endorse any third parties referenced on this site. When you invest, your money is at risk and it is possible that you may lose some or all of your investment. Past performance is not a guarantee of future results. Historical returns, hypothetical returns, expected returns and images included in this content are for illustrative purposes only.