Finance for Humans

How to Be Smart with Your Tax Refund (and Still Buy Stupidly Expensive Things)

Be a grown-up this year and invest in Future You. Then be a kid and buy something that makes you happy.

Wealthsimple makes powerful financial tools to help you grow and manage your money. Learn more

Congratulations, you paid your taxes on time. (You did, right?) And now maybe you’re counting the days until you get that refund check. Hooray, you may be thinking. Free money! I can do whatever I want with it and not feel bad because it’s free free free. But as much as you might want some stupidly expensive Raptors tickets or seven $200 pairs of sneakers in rainbow colours, the thing you should be most excited about is socking that money away in your RRSP right now. And yeah, we mean it when we say excited. Here’s why. (Make sure you read to the end: Maybe you can buy those Raptors tickets after all.)

Sign up for our weekly non-boring newsletter about money, markets, and more.

By providing your email, you are consenting to receive communications from Wealthsimple Media Inc. Visit our Privacy Policy for more info, or contact us at privacy@wealthsimple.com or 80 Spadina Ave., Toronto, ON.

You’re Going to Want to Max Out Anyway

You might remember that we covered this back in February. But in case you missed it: You really should make sure you shave off 18% of your income (up to $25,370, the maximum allowed by law) to put in your RRSP by next year’s deadline. And better yet, don't wait until next year's deadline. Because the earlier you start, the more you'll reap the benefits of man's greatest invention, compound interest.

It Lowers Your Tax Liability

Let’s say you got $7,346 back from the government. Sure, overpaying your taxes was kind of an interest-free loan to the government. Don’t worry about that, because you’re going to help your next year’s tax bill right now: By putting that $7,346 tax refund into an RRSP, you’re automatically lowering your income taxes—and you’ll earn money on that money if the market goes up.

Recommended for you

Is This the Year to Try Wealthsimple Tax? (Um, Probably. Yes)

Finance for Humans

OMG You’re Having a Baby! (A Guide to That and Other Big Life Moments That’ll Affect Your Taxes)

Finance for Humans

The Budget for People Who Hate Budgeting (and Also Want a Bidet)

Finance for Humans

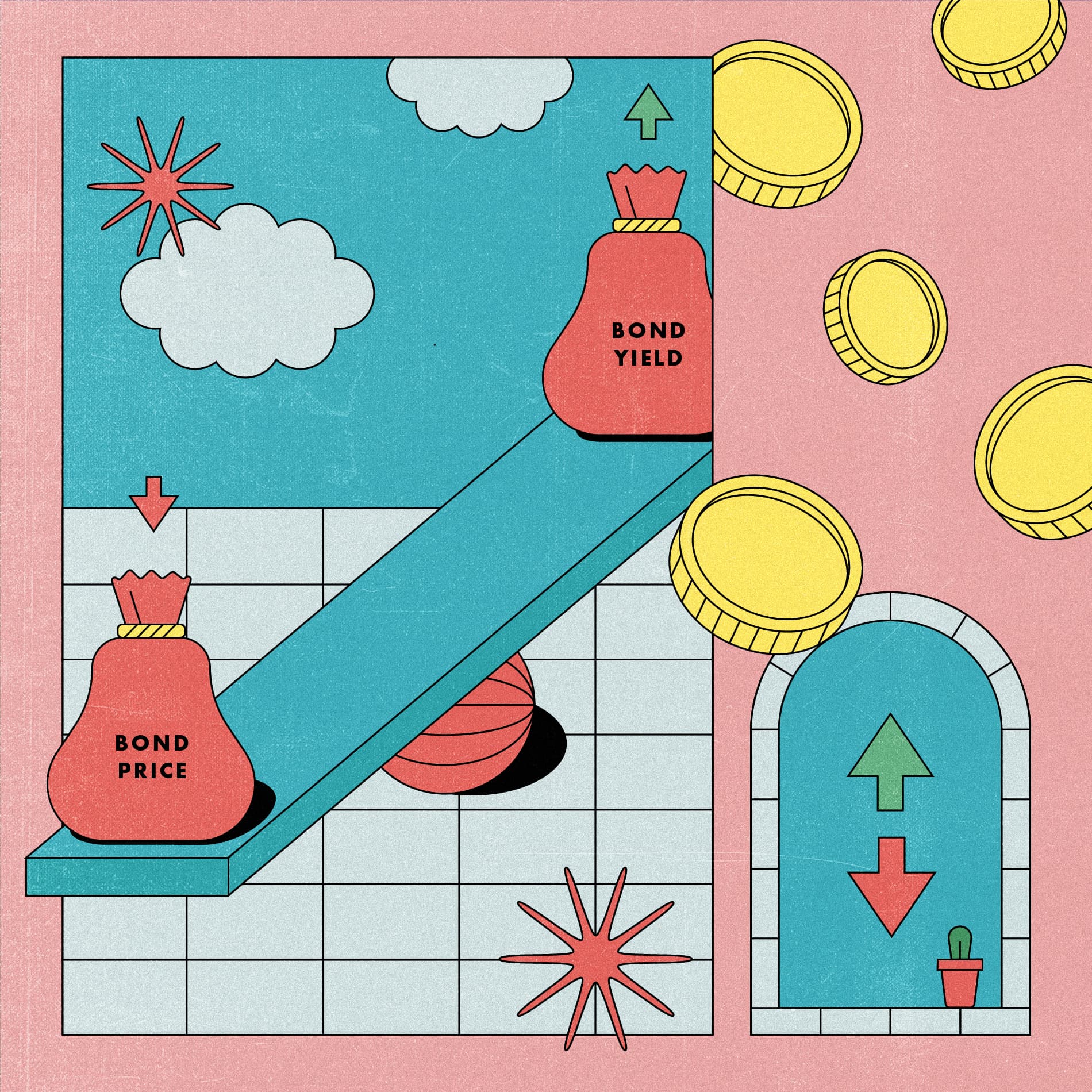

The Bond Market Fell, Hard. An Explainer for Normal Humans

Finance for Humans

It Makes You a Financial Genius

According to Stats Canada, fewer than 20% of Canadians contributed to their RRSPs in 2011. Don’t be that guy. If you’re even a little responsible now, it lets you be more irresponsible later.

It Helps Future You Even if It’s Only a Few Dollars

A lot of Canadians think you need to have lots of cash to invest to make it worthwhile. We can’t say it enough: At Wealthsimple, no amount is too small. Because of our investing technology, we can diversify any size account, whether it’s a dollar or a million. You have to start somewhere, so get in the right habits now, and over time you can make those contributions larger.

You Can Still Blow Some of the Free Money

At Wealthsimple, we’re all about fostering healthy spending and investment habits. And what builds better habits than rewarding good behaviour? So if you’ve put, say, $1,000 into your RRSP and you have $300 left, go ahead and get tickets to a Raptors playoff game. Who knows whether they’ll make it this far next year, and investing in experiences isn’t such a bad way to spend money either. Plus, if you reward yourself every time you save, it’ll incentivize you to save even more down the line.

Wait, don’t tell us you haven’t opened an RRSP with us. What are you waiting for? Sign up now.

Written By

The Editors

Wealthsimple's education team is made up of writers and financial experts dedicated to making the world of finance easy to understand and not-at-all boring to read.