Money & the World

The Sandwich Generation Is Getting Smushed

Middle age has long been a pricey phase of life. Now, thanks to the rising costs of child and parental care, it’s breaking budgets — and revealing a lot about Canada

Wealthsimple makes powerful financial tools to help you grow and manage your money. Learn more

Mireille’s induction into the sandwich generation came in 2021, with a worried phone call from her mother’s friend. Mireille’s mother, Colleen, a retired professor in Guelph, Ont. — both of their names have been changed — had always been the one to drive her friends to exercise class, but now she was forgetting her way home. Maybe, the friend gently suggested to Mireille, she shouldn’t be driving anymore?

That call five years ago changed Mireille’s life, triggering a cascade of medical appointments, hospital stays, and retirement-home tours, all squeezed around her two teens’ schedules. And work. And, theoretically, sleep.

“It’s like I’m living in two worlds,” says Mireille, 48. In one, she’s a flight attendant, making round trips from Toronto to Vancouver and L.A., while also raising a family. In the other, she trails her mom, now 79, around the house as if she were a toddler, worried she might fall or misplace something.

A quarter of all Canadians — 13.4 million people — provide at least some unpaid care for a parent or child each year. A growing subset of nearly 2 million people provide unpaid care for both. Mireille is now a verified member of this club, known as “the sandwich generation” or “the crunch generation,” thanks to their precarious role supporting two households.

They’re mostly folks in their late 30s through early 60s, and all the giant, suffocating responsibilities, new and old, on these midlifers have made them more stressed about their finances than any other group of Canadians, according to surveys. We found out how they’re getting squeezed and what they’re doing about it, so the rest of us can learn from their experience.

A care double whammy is breaking budgets

Middle age has long been an extra-pricey stage of life, what with kids and all. What’s new is that women today are having babies later and later, while their boomer parents are living longer than past generations, putting overlapping burdens on Sandwichers.

Take Debbie, an insurance underwriter from Newmarket, Ont. She looks out for her parents and her in-laws, all of whom collect pensions. But when her father needed cataract surgery last year, his insurance plan would only cover his nearsighted correction or his farsighted correction, not both. So Debbie paid $8,000 out of pocket. Then her parents’ central AC broke ($7,000). Then her father-in-law needed hernia surgery, and they opted for private care ($5,000) rather than force him to wait months for the publicly insured option.

“I don’t exist,” Debbie joked to me wryly. “I only exist to assist the kids and the parents.”

Then there’s the other side of the midlife money sandwich: children. For medium-income households that earn between $83,000 and $136,000 annually, raising a child — just one of them — from birth to age 18 now costs around $374,000. That’s up from $167,000 in 2004, far outpacing inflation. And if your household makes more than $136K, you’ll likely pay way more, since child-rearing expenses rise in lockstep with income.

Perhaps the biggest hitch with children is all the extra space they need to grow; hence, middle-aged Canadians spend more annually on housing — $31,600 — than any other group.

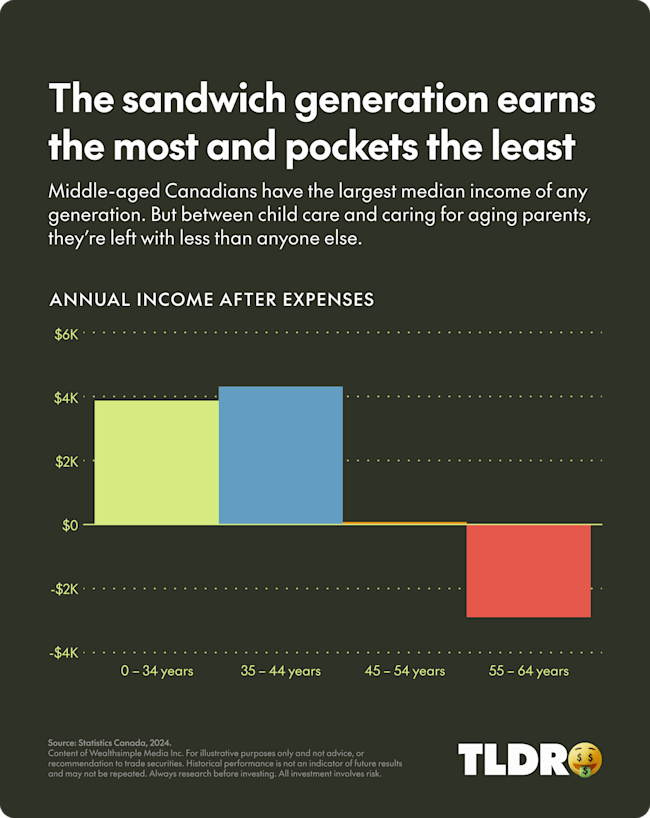

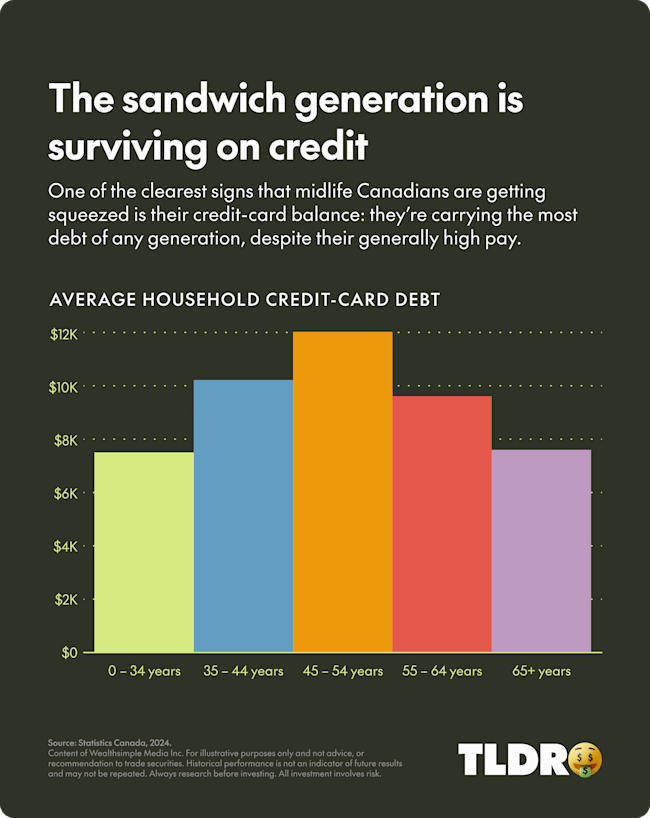

Thanks to all these costs, Canadians aged 40 to 54 have endured the biggest jump in spending over the past dozen or so years, according to StatCan. They have by far the highest living expenses, at more than $141,000 annually per household. And they hold the highest household credit-card debt of any age group — an average of $12,000 — even though middle age is when wages typically peak.

The indirect costs are just as painful

Unpaid caregivers provide roughly three hours of care for every one hour of professional care, and two-thirds say it hurts their careers. Last year, Mireille missed weeks of work while caring for her mother, and while she was away, her husband had to scale back on his IT business so he could pick up the slack at home. Altogether, their combined income dropped from $220,000 in 2024 to $100,000 in 2025.

But the hardest part, Sandwichers say, is the mental toll

All the appointments, all the calendar invites, all the schlepping. It adds up: 86% report feeling depressed or anxious, in addition to other negative health effects.

Debbie used to roll her eyes when friends warned her that the spontaneity in her life would vanish once she had kids and as her parents aged. Now she says that by the time January rolls around, “my life is planned literally up to the end of September.” She counts herself lucky to have paid vacation and a standing monthly dinner with friends.

Sandwichers are not (entirely) giving up

The remarkable thing about middle-aged Canadians is that, despite all the crunching and sandwiching, they’re still saving about $15,000 a year on average. That’s less than millennials’ $22,000, but still meaningful. If you start saving at 45 (and let’s hope you begin before that) with $0 and invest $15,000 annually until you retire at 65, you could end up with more than $500,000 (assuming a 5% annual return). Point being: modest contributions add up. “I think you should just save whatever you can and hope for the best,” Debbie says.

Another advantage middle-aged folks have is that many will inherit substantial sums as part of the largest intergenerational wealth transfer in Canadian history. They also have some of the highest rates of homeownership in Canada. (And 30-somethings aren’t far behind.) Mireille’s husband tries to ease her fears about retirement by reminding her that they could just sell their place to fund their golden years. But then what, she wonders? “We’re not going to live in a tent.”

Perhaps they can lean on their children to figure out a solution. ♦

Brennan Doherty assisted with data reporting.

Written By

Katherine Laidlaw

Katherine Laidlaw is an award-winning journalist based in Toronto. She writes for WIRED, Outside and The Atlantic, among other publications.